Many American families think of currency strength as something decided far away, by central banks, trade officials, and foreign governments. In daily life, the concern feels much closer. It shows up in grocery bills, retirement statements, higher borrowing costs, and the fear that years of disciplined saving may not buy as much for the next generation.

China’s gold buying belongs in that conversation. Official reports show one version of Beijing’s gold position. Market analysts argue the real number may be far larger. The gap matters because gold is not only a metal. For governments, it is a reserve asset that does not depend on another country’s promise to pay.

When a major foreign power reports continued additions to physical bullion, U.S. retirement savers may want to understand how reserve diversification fits into the broader monetary environment. Reported gold buying alone does not confirm how much China is reducing dollar-based holdings or what that means for the dollar.

Understanding that gap means examining how the People’s Bank of China (PBoC) reports its holdings, how the Shanghai Gold Exchange (SGE) fits into China’s physical gold market, and what reserve-diversification trends may mean for families trying to protect wealth in a more fragile monetary environment.

Key Takeaways:

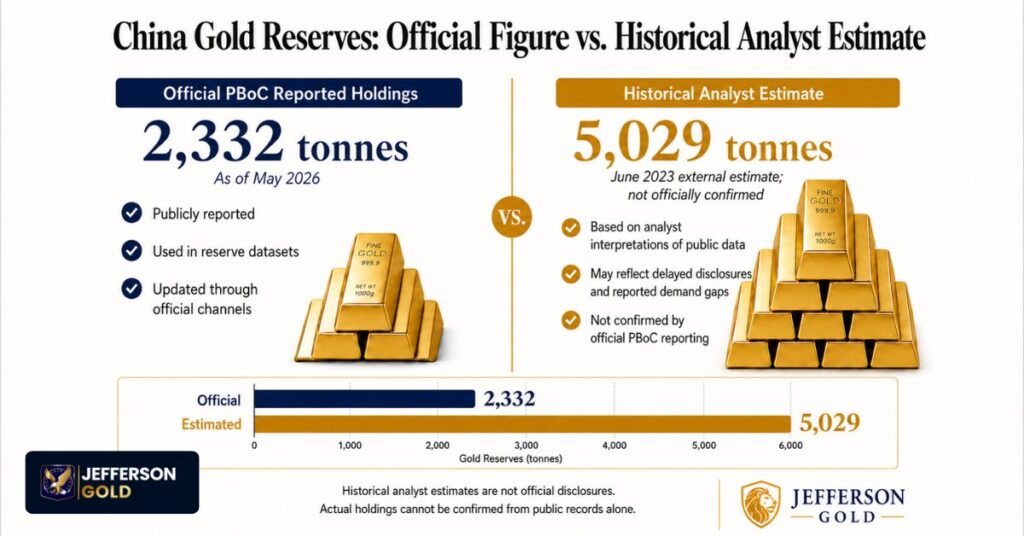

- China’s official gold holdings reached about 2,332 tonnes in May 2026 after the PBoC reported its 19th straight monthly increase.

- An outside analyst estimated that China may have controlled about 5,029 tonnes of monetary gold by June 2023. This was a model-based estimate, not an official PBoC disclosure, and it should not be treated as a current verified reserve figure.

- The gap between official and estimated holdings is the core issue: reported reserves are visible, while analyst estimates rely on delayed disclosures, public trade data, reported central-bank demand, and other information that cannot confirm a hidden total.

- The World Gold Council’s 2026 survey found that 89% of reserve managers expect global central-bank gold holdings to rise, 45% expect their own holdings to increase, and 74% expect the U.S. dollar’s share of global reserves to decline over five years.

- For U.S. retirement savers, the lesson is not to copy a foreign government. It is to recognize the same structural signal: major monetary authorities are treating physical gold as a protection layer against currency, sanctions, and reserve-system risk.

Mapping the China Shadow Gold Reserves Tracker

![]()

A China shadow gold reserves tracker compares officially reported bullion holdings with estimated true holdings based on public reserve data, unreported central-bank buying, trade-flow analysis, and Shanghai Gold Exchange activity. The goal is not certainty. It is to measure the likely gap between what Beijing reports and what it may actually control.

The key phrase is Beijing physical bullion holdings, not merely “gold demand.” China has jewelry demand, bar and coin demand, industrial use, domestic mine supply, and central-bank reserves. The tracking challenge is separating ordinary commercial flows from state-linked reserve accumulation.

Officially, the PBoC reported about 2,332 tonnes of gold in May 2026. 1 That number is useful because it is visible, repeated in public datasets, and comparable with other countries. It is also incomplete according to analyst models.

Nieuwenhuijs estimated China’s official gold reserves at 5,029 tonnes by the end of June 2023, but this remains an external estimate, not a central-bank disclosure. 2

Limits of Reserve Estimates

Analyst estimates of China’s possible gold holdings are built from public information, including official reserve updates, reported central-bank demand, trade data, domestic production, and patterns of delayed disclosure. These methods can identify questions worth examining, but they cannot establish a confirmed total without official documentation.

For that reason, the difference between reported reserves and analyst estimates should be understood as an area of uncertainty rather than proof of a hidden figure.

Why Central Banks May Disclose Gold Purchases Gradually

Analysts have suggested several possible reasons why a central bank might disclose gold purchases gradually, including market sensitivity, reserve-management discretion, and the political value of keeping reserve composition private. However, the PBoC has not publicly confirmed a motive for any reporting pattern, so these explanations should be treated as interpretation rather than established fact.

Gold also speaks to the risk of external control. The 2022 freezing of Russian foreign reserves showed that foreign-currency reserves can become politically exposed when held inside another country’s legal and settlement system. Brookings reported that Russian foreign-exchange reserves held by the United States and its allies were frozen after Russia invaded Ukraine, with estimates often placing the frozen amount near $300 billion. 3

The freezing of Russian foreign reserves intensified global discussion about sanctions exposure, custody risk, and access to reserves held abroad. It may be one factor that reserve managers consider alongside liquidity, diversification, domestic policy, and geopolitical risk.

That does not mean gold is risk-free. It has storage costs, price swings, custody questions, and verification requirements. But for sovereign states, it has one feature that paper claims do not: it does not require another government to honor a payment promise.

Operational Mechanics of Beijing Physical Bullion Holdings

China’s gold system has two visible channels and one less visible channel. The first visible channel is domestic mine supply. China has long been one of the world’s major gold producers, and domestic production can feed commercial demand without crossing a border.

The second visible channel is commercial import and clearing activity. The Shanghai Gold Exchange is central to this structure. SGE materials describe it as a marketplace for gold trading, clearing, delivery, and vaulting services in China’s gold market. 4

Outside analysts have proposed that delayed disclosures and unreported official-sector buying may make China’s total gold holdings difficult to assess from public records. These are model-based interpretations, not verified descriptions of a specific acquisition channel or ownership structure.

That matters because trade and customs records do not always reveal the final owner. A shipment may appear as commercial gold, move through banks, refiners, or vaulting networks, and still leave analysts unable to confirm whether it ended as private demand, commercial inventory, or state reserve accumulation.

Public Reserves vs. Shadow Reserves

The table below separates what China reports publicly from what analysts estimate may exist beyond official reserve disclosures. The public number is clean but may be incomplete, while the estimated number is broader but less certain. Readers should keep that distinction clear.

| Metric | Publicly Reported Reserves | Estimated Shadow Reserves |

| Reporting Source | Official PBoC Reserve Disclosures | Analyst Estimates, Trade-Flow Gaps, Unreported Buying Models |

| Current Scale | About 2,332 Tonnes Officially Reported in May 2026 | A Historical External Estimate of 5,029 Tonnes for June 2023; Not Officially Confirmed and Not a Current Verified Total |

| Visibility | Public and Trackable | Inferred, Not Officially Confirmed |

| Reporting Frequency | Periodic Official Updates | No Formal Reporting Schedule |

| Transparency | Included in Public Reserve Data | Outside Standard Transparency Ledgers |

| Storage Visibility | Part of Official Reserve Framework | Inferred From Public Data and Analyst Models; Not Officially Confirmed |

| Strategic Function | Public Confidence and Reserve Reporting | Possible Strategic Rationale Cited by Analysts; Not Officially Confirmed |

| Main Limitation | May Not Show the Full Position | Cannot Be Confirmed from Public Records Alone |

The De-Dollarization Threat and Cross-Generational Wealth Insulation

The de-dollarization trend does not mean the dollar disappears. It reflects gradual diversification away from dollar-denominated assets. The relationship between gold accumulation and dollar demand is not mechanical. Outcomes depend on interest rates, fiscal policy, inflation, trade flows, energy prices, and central-bank decisions.

The same reserve trend also connects with broader discussions about BRICS expansion, non-dollar trade settlement, reserve diversification, and central-bank gold buying. However, BRICS is not a unified currency bloc and does not operate a shared currency system.

A major reserve holder may earn dollar balances through trade and choose to diversify part of its reserves across gold, currencies, bonds, and other assets.

Changes in reserve composition can influence long-term demand for reserve assets, but the effects on the U.S. dollar depend on many variables, including interest rates, fiscal policy, growth, trade flows, inflation, and market confidence.

For households, the practical issue is not that one country’s gold purchases automatically cause a dollar decline. It is that global reserve diversification is one of several structural trends worth understanding when considering long-term purchasing-power and retirement risks.

The World Gold Council’s 2026 central-bank survey supports the broader pattern. It found that 89% of surveyed reserve managers expected global central-bank gold holdings to rise over the next 12 months, 45% expected their own institution’s gold holdings to increase, and 74% expected the dollar’s share of global reserves to be lower in five years. 5

That survey does not predict a sudden dollar crisis or prove how any individual central bank will act. It shows that many reserve managers expect official gold holdings to rise and expect the dollar’s reserve share to be lower over time. For families, the practical lesson is to understand the role that different assets can play during periods of monetary and geopolitical uncertainty.

This concern also fits within the broader wealth-protection framework covered in The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

Jefferson Gold’s asset insulation strategies guide helps explain why physical precious metals may serve as one layer of family wealth preservation when confidence in paper systems comes under pressure.

For readers who want the process side, Jefferson Gold’s direct delivery and account purchase steps guide explains how buyers can learn about physical gold and silver purchases.

What the Shanghai Gold Exchange Reveals and What It Does Not

The Shanghai Gold Exchange is not proof of hidden PBoC buying by itself. That boundary is important. The SGE is a major domestic clearing and delivery platform. It helps show the scale of Chinese physical metal demand. It also shows how gold can move through a regulated domestic system where commercial and institutional flows are deeply connected.

But the SGE does not neatly tell an outside reader which bar is held by a private buyer, a commercial entity, a state-linked firm, or the central bank. That is why SGE data must be read as part of a wider tracking system, not as a standalone answer.

A reasonable tracking framework looks at:

- Official PBoC reserve updates.

- Net central-bank buying reported by global gold authorities.

- Unreported central-bank demand gaps.

- Chinese domestic production.

- Import and export data from key transit hubs.

- Shanghai Gold Exchange withdrawals and clearing patterns.

- Analyst estimates from specialists who track monetary gold separately from commercial gold.

This is the value of the “tracker” concept. It does not claim perfect knowledge. It creates a disciplined way to compare reported data with market behavior.

Why Physical Bullion Matters When Reserve Systems Change

China’s reserve behavior points to a larger truth: physical assets and paper claims carry different risks. A Treasury bond depends on issuer payment. A bank balance depends on banking-system access. A brokerage statement depends on platform, custodian, market, and settlement access. Physical bullion still has price and custody risks, but it is not the same kind of claim.

That distinction helps explain why central banks hold gold. It also explains why families concerned about retirement savings, inflation, and inheritance protection often want to understand physical gold and silver before the next major shock.

This does not mean every family should make the same choice. It means the topic deserves serious review. A person who has worked for decades to build retirement savings should understand the difference between owning a physical asset and owning a claim inside a paper-based system.

Jefferson Gold can support that education by helping customers understand available physical gold and silver products, account-based purchase paths, and secure delivery or storage-related options. Readers who want to ask direct questions can use Jefferson Gold’s Contact Us page to request a private conversation with a specialist.

Final Thoughts

China’s reported gold purchases, together with outside estimates of possible unreported holdings, have intensified attention on how reserve managers balance gold, currencies, and debt securities.

These developments do not establish a single future outcome for the dollar. They do show why reserve diversification remains an important part of global monetary analysis during periods of geopolitical and economic uncertainty.

American families do not need to predict every move China makes. They only need to understand the signal. As central banks continue to review how gold, currencies, and debt securities fit within their reserves, retirement savers have reason to understand how tangible precious metals may fit within broader family wealth-preservation planning.