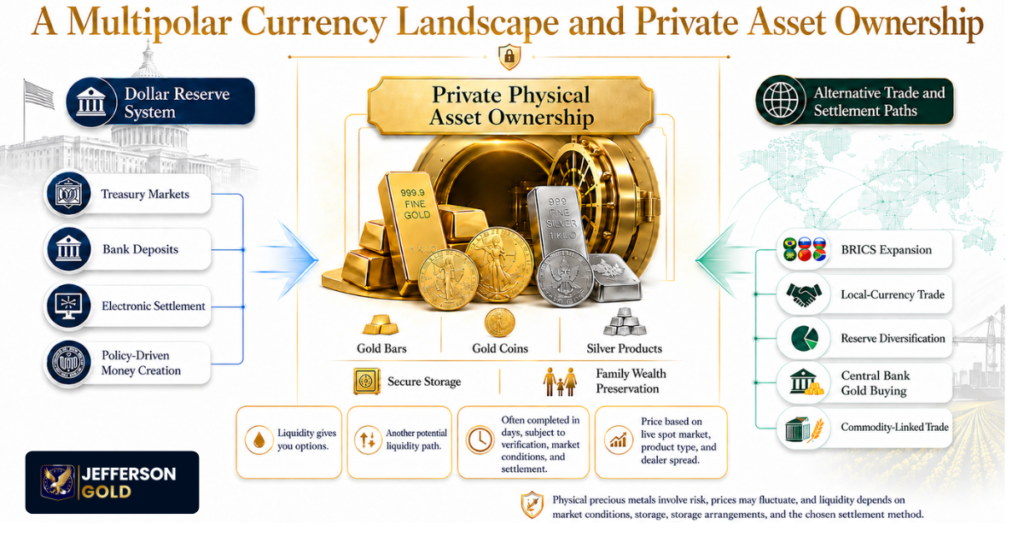

BRICS has expanded beyond its original five members and now includes Brazil, Russia, India, China, South Africa, Saudi Arabia, Egypt, Ethiopia, Iran, the United Arab Emirates, and Indonesia. The group is not a single-currency system, but its members have shown increasing interest in local-currency trade settlement, reserve diversification, and financial arrangements that reduce reliance on any one currency.

This does not mean the U.S. dollar is disappearing. The dollar remains the leading currency in allocated global foreign exchange reserves and remains central to global trade and financial markets. The more practical question for retirement savers is how changes in reserve preferences, trade settlement, inflation, and interest rates may affect long-term purchasing power.

For a broader overview of long-term wealth preservation during periods of economic uncertainty, read The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

Key Takeaways:

- The global monetary system is moving toward a more multi-polar structure as BRICS and other trade partners seek more non-dollar settlement paths.

- The U.S. dollar remains the world’s leading reserve currency, but its share of allocated global reserves has moved lower over time.

- Central banks have been steady gold buyers in recent years, showing renewed interest in physical gold as a neutral reserve asset.

- Physical gold may help families think about purchasing power, direct ownership, and long-term wealth preservation outside purely paper-based claims.

- Gold is widely traded, but selling physical metals still depends on dealer availability, verification, market conditions, storage arrangements, and bid-ask spreads.

The Mechanics of Petro-Dollar Recalibration

The petrodollar system is not a formal treaty that freezes the world in place. It is a network of habits, pricing practices, financial rails, security relationships, and Treasury-market depth. Oil and other major commodities have long been priced largely in dollars because buyers and sellers trust the liquidity and reach of dollar markets.

When more trade partners test local-currency settlement, commodity-linked payment systems, or regional clearing structures, the dollar’s role can narrow at the margin. That does not require a collapse. A small change in reserve behavior, repeated over years, can still matter.

The IMF’s COFER data shows the U.S. dollar remains the largest currency in allocated official foreign exchange reserves, but its share has moved lower from earlier decades.1

That steady change is why central bank behavior deserves attention. If sovereign institutions are looking for assets that do not depend on another country’s currency promise, gold becomes part of the discussion.

Learn more about the factors behind central-bank gold demand in Why Central Banks Are Accumulating Physical Gold Ahead of BRICS Expansion.

Systemic Inflation vs. Physical Asset Attributes

Inflation Protection with Gold begins with a simple concern: paper money can be expanded by policy, while physical gold cannot be created by vote, decree, or central-bank balance sheet expansion. Gold is dense, durable, scarce, and widely recognized, with a long history as a store of value across monetary systems.

That does not make gold risk-free. Prices move, premiums vary, and transaction costs exist. But physical bullion is different from a bank deposit, bond, ETF share, or digital account balance because those assets depend on issuers, custodians, market systems, and account access. Physical gold bars and coins, when owned directly or held through appropriate storage arrangements, are tangible property rather than a paper claim.

World Gold Council survey data shows that central banks continue to view gold as an important reserve asset. Its 2026 survey found that 89% of respondents expected global official gold reserves to increase over the following 12 months, while 45% expected their own institution’s gold holdings to rise.2

For private buyers, the lesson is not that central banks and families have the same needs. It is that gold remains relevant in discussions about reserve diversification, currency uncertainty, sovereign debt, and long-term purchasing power.

Understanding Counterparty Risk in Paper Liabilities

Counterparty risk means depending on someone else to perform. A bank deposit depends on the bank and the insurance framework. A bond depends on the borrower. A fund share depends on its structure, custodian, market access, and settlement systems. A brokerage account depends on electronic networks and institutional operations.

Physical bullion reduces some of those dependencies because it is not another party’s repayment promise. Still, it should not be described in absolute terms. Storage choice, insurance, documentation, transportation, dealer verification, and resale process all matter. The more precise point is this: physical gold does not rely on the solvency of a bank or issuer in the same way paper claims do.

That is why many families look at asset insulation strategies when they are trying to understand how tangible assets may fit into a long-term wealth preservation plan.

Historical Case Study: Structural Monetary Realignments

The early 1970s remain the most important modern U.S. example of monetary change. On August 15, 1971, President Richard Nixon suspended the dollar’s convertibility into gold for foreign monetary authorities, closing the gold window and ending the central link that had anchored the Bretton Woods system. 3

The result was not immediate disorder, but the structure of money changed. The dollar was no longer tied to gold at a fixed official exchange rate. The 1970s then became a decade marked by inflation, oil shocks, weak confidence, and pressure on savers. Families holding only dollar-denominated paper assets had to live with the real-world effects of rising prices. Rising prices and monetary instability affected households differently depending on their income, savings structure, debt, and exposure to tangible or financial assets.

The lesson still matters today because monetary systems do change. Today’s BRICS-dollar tension is not a copy of the 1970s, but the family-level concern is familiar: when confidence in money changes, purchasing power becomes the issue.

Strategic Frameworks for Long-Term Asset Insulation

Wealth Preservation Through Gold is not about predicting tomorrow’s headline. It is about understanding asset characteristics before stress arrives. Physical gold ownership solutions usually center on direct ownership of coins and bars for personal control or professional storage, as well as specialized precious metals retirement account structures when appropriate.

Readers who want to understand how to open a gold IRA account should review the rules carefully and speak with qualified professionals before making decisions. IRS guidance states that certain gold, silver, platinum, or palladium bullion may be held in individually directed retirement accounts if it meets required fineness standards and is kept in the physical possession of a bank or approved non-bank trustee. 4

The core distinction is practical. Physical bars and coins are tangible. ETFs, derivatives, and mining shares are paper or electronic claims tied to institutional systems. They may have a role for some people, but they are not the same as direct ownership of bullion.

Physical Precious Metals and Retirement Planning

Physical gold does not guarantee a retirement outcome or remove market risk. However, it may help retirement savers understand the practical difference between tangible metals and holdings that exist only as digital balances or paper claims.

Gold bars and coins are physical, durable, and globally recognized. Silver may also interest some buyers because of its monetary history and industrial demand, though it can be more volatile.

For many U.S. families, the key questions are practical: where the metals would be stored, how products are verified, what premiums apply, and how a future sale would work. Gold is widely traded, but physical liquidation still depends on product type, dealer availability, authentication, market hours, storage arrangement, settlement method, and bid-ask spreads.

Cross-Generational Asset Insulation

Cross-generational asset insulation is about passing down purchasing power, not just account statements. A physical gold coin or bar is easy to understand because it is not abstract. It is a tangible property with a long history of recognition.

That matters for families. A child or grandchild may not fully understand central bank policy, reserve currency blocs, or Treasury auctions. But they can understand that gold has been valued across countries, languages, and political systems for thousands of years.

This does not mean every family needs the same approach. A household in Florida may have different needs from one in Texas, the Midwest, or a conservative pocket of California. Age, retirement timeline, existing savings, storage comfort, and family goals all matter. The educational goal is to help buyers ask better questions before choosing any path.

Distinguishing Asset Classes: Physical Bullion vs. Synthetic Paper

A gold ETF may track the price of gold, but it is still a financial product inside an institutional framework. Mining shares can rise or fall based on company management, labor costs, energy costs, jurisdictional issues, and equity-market sentiment. Futures contracts involve leverage, expiration dates, margin rules, and exchange systems.

Physical bullion is different. It is not a share of a company. It is not a promise to deliver later. It is metal that can be held, stored, verified, and sold through bullion dealers. That difference is why families concerned about currency blocs often focus on physical ownership rather than only price exposure.

| Asset Attribute | Paper-Denominated Instruments | Physical Sovereign Bullion |

| Counterparty Exposure | Depends on Issuer, Custodian, Platform, or Borrower | Lower Reliance on Issuer Promises When Owned Directly |

| Account Access Risk | May Depend on Banking, Brokerage, or Electronic Networks | Depends on Custody Choice, Storage Access, and Documentation |

| Purchasing Power History | Exposed to Fiat Expansion and Rate Cycles | Long Record as a Store of Value Across Monetary Systems |

| Liquidity Process | Subject to Market Hours and Platform Rules | Subject to Dealer Protocols, Verification, Spreads, and Settlement |

| Family Transfer Clarity | Often Requires Account Paperwork and Beneficiary Handling | Tangible Property, but Still Requires Careful Estate Planning with Qualified Professionals |

Conclusion

The growth of BRICS, non-dollar trade settlement efforts, and the continued strength of the U.S. dollar do not create a simple story of one side winning and the other losing. The dollar still has depth, liquidity, trade reach, and institutional strength. But the world is clearly testing alternatives.

For American families, the responsible question is not whether the dollar disappears. It is whether all long-term savings should depend on the same paper system at the same time that central banks are adding more gold to their own reserves.

Physical gold and silver do not remove every risk. They do not promise returns. They do not replace professional planning. But they can give families something paper assets cannot: tangible ownership of a recognized store of value that has outlasted many monetary systems before this one.

To learn more about buying physical precious metals, storage options, and retirement-account documentation, speak with a Jefferson Gold specialist or request an educational guide.