Interest in bank bail-in protection has grown among retirement savers concerned about banking stability, inflation, rising national debt, and long-term access to their savings. Many families want to understand what could happen to money held inside financial institutions during periods of severe banking stress.

Modern banking systems now operate under resolution frameworks designed to reduce reliance on taxpayer-funded rescues and help stabilize distressed institutions.

For many Jefferson Gold readers, the bigger question is whether all family wealth should remain inside the same financial system. This concern appears throughout Jefferson Gold’s educational materials on banking risk, inflation, debt, and long-term wealth preservation.

Physical gold is often part of that discussion because it is tangible property rather than a bank deposit. While gold ownership involves considerations such as storage, verification, pricing, and liquidity, it exists outside the banking system’s deposit-liability structure.

For a broader perspective on navigating economic uncertainty, readers may also find value in The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

Key Takeaways:

- Modern banking resolution frameworks differ significantly from those used before the 2008 financial crisis.

- FDIC insurance provides important protections, but coverage limits remain important.

- Physical gold held directly is not recorded as a bank deposit and does not depend on the financial condition of a commercial bank in the same way a checking or savings account does.

- Many retirement savers view physical precious metals as a way to hold a portion of their wealth in tangible form.

- Understanding how deposits, insurance coverage, and resolution frameworks operate can help families make more informed decisions.

The Evolution of Institutional Resolution Frameworks

For decades, major banking disruptions often led to discussions about taxpayer-funded bailouts. After the global financial crisis, policymakers sought alternatives that would place greater responsibility on institutions and reduce dependence on public rescue programs. The result was a move toward formal resolution frameworks designed to stabilize distressed institutions while preserving essential financial services.

In the United States, Title II of the Dodd-Frank Act established the Orderly Liquidation Authority. According to the FDIC, this framework serves as a backstop for resolving certain large financial companies when traditional bankruptcy may not adequately protect financial stability. 1

In Europe, regulators introduced the Bank Recovery and Resolution Directive (BRRD), which established a framework for handling distressed banks and covered financial entities. 2

Rather than focusing on technical regulatory language, retirement savers should focus on the practical lesson: modern banking systems now operate under formal resolution procedures that may affect how institutions are handled during periods of severe stress.

How Modern Banking Laws Can Affect Depositor Claims

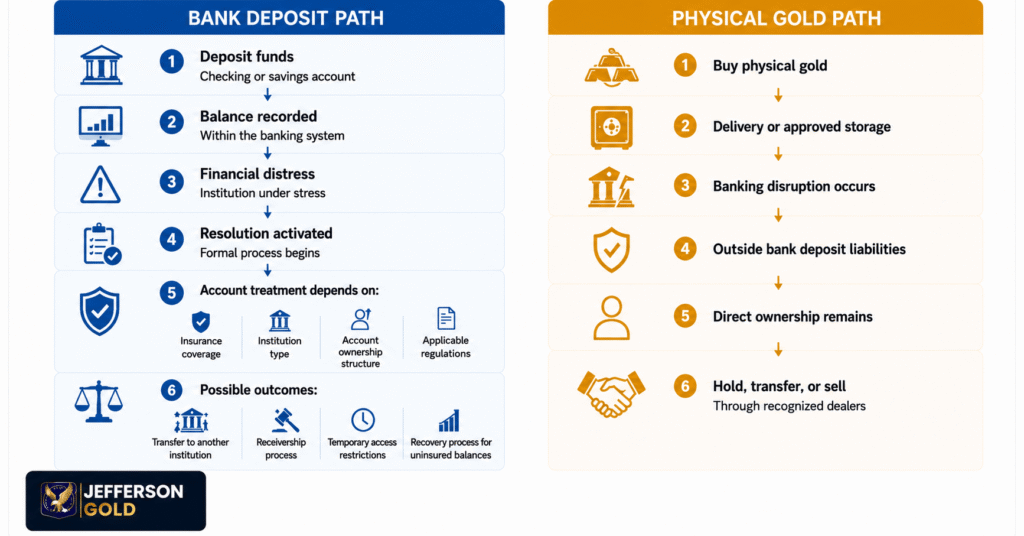

Many Americans view checking and savings accounts as secure places to store money. In practice, the relationship between a financial institution and an account holder is more complex.

When funds are deposited into a bank account, the account holder receives a claim against the institution for the recorded balance. The institution then uses deposits as part of its broader funding structure.

FDIC insurance exists specifically to protect covered deposits within established limits. However, balances above those limits may be treated differently if a financial institution enters receivership. 3

This distinction is one reason some retirement savers choose to hold a portion of their wealth in physical assets. Tangible assets such as physical gold are not bank deposits and are not dependent on the claims process associated with a failed institution.

For readers seeking a more detailed explanation of these legal relationships, see: How Modern Banking Laws Turn Depositor Cash into Bank Equity.

Operational Vulnerability

One of the biggest misconceptions surrounding banking failures is that the only concern is permanent loss. In reality, delays, administrative procedures, uncertainty, and restricted access can create significant challenges even when protections exist.

The FDIC notes that insured deposits are generally made available quickly after a bank failure. Uninsured amounts may be subject to a recovery process tied to the institution’s remaining assets. 4

For families approaching retirement, timely access to savings can be just as important as the amount ultimately recovered. This is one reason Jefferson Gold frequently discusses the role of tangible assets within a broader wealth preservation strategy.

What the Bank Recovery and Resolution Directive Means for Your Savings

The Bank Recovery and Resolution Directive (BRRD) is one of the most widely discussed examples of modern banking resolution policy. Its purpose is to provide authorities with tools for addressing distressed institutions while preserving critical banking functions.

Although BRRD applies to European institutions, its broader significance lies in demonstrating how regulators around the world have developed formal procedures for handling financial stress.

For American retirement savers, the key takeaway is not the specific details of European law. The more important lesson is that banking institutions operate within regulatory frameworks that may affect access, recovery procedures, and institutional restructuring during periods of severe distress.

For a more detailed examination of international resolution frameworks, see: What the Bank Recovery and Resolution Directive Means for Your Savings.

How Physical Gold Creates Separation from Bank Deposits

This is where the discussion shifts from banking structures to wealth preservation. Physical assets have historically occupied a unique place within wealth preservation discussions because they exist independently of many financial intermediaries.

Jefferson Gold’s educational materials frequently emphasize that physical gold ownership is fundamentally different from holding a bank balance. A bank account represents a claim within the financial system. Physical gold represents direct ownership of a tangible asset.

Physical gold ownership does not eliminate risk. Prices fluctuate. Storage requires planning. Selling physical metals involves normal market procedures. However, direct ownership creates a structural separation from the banking system that many retirement savers find attractive.

Jefferson Gold helps customers learn about physical gold and silver purchases, direct delivery and account purchase steps, and available storage considerations.

Legal Autonomy of Tangible Property

Physical gold held directly is tangible personal property. Unlike a bank deposit, it is not recorded as a liability on a commercial bank’s balance sheet. Many families concerned about inflation, banking uncertainty, debt levels, and preserving purchasing power choose to learn more about physical precious metals because of this distinction.

Many families review broader asset insulation strategies because they value the separation between tangible precious metals and traditional financial institutions.

Jurisdiction Diversification: Moving Physical Gold to Stable, Offshore Vaults Outside Local Control

One challenge with traditional bank deposits is that they are generally tied to a specific institution and jurisdiction. Access to those funds depends on the rules, regulations, and operational status of that banking system. Physical precious metals can be held in different ways, including personal possession, domestic storage facilities, and certain international vaulting arrangements.

Many wealth preservation buyers focus on diversification across asset types. Others also think about diversification across jurisdictions. The goal is not to avoid regulations. Instead, it is often about reducing dependence on a single financial system, institution, or geographic location.

Some families consider offshore storage because it may provide an additional layer of geographic separation. However, offshore storage is not automatically appropriate for every situation. Storage agreements, insurance arrangements, access procedures, reporting obligations, and local laws should all be reviewed carefully.

This discussion is ultimately about flexibility. During periods of financial uncertainty, some families prefer knowing that not all assets are concentrated within the same banking network or jurisdiction.

For a deeper discussion of international storage considerations, see: Jurisdiction Diversification: Moving Physical Gold to Stable, Offshore Vaults Outside Local Control.

Liquidity in a Crisis: How to Safely Sell Physical Gold Coins When Banks Implement Withdrawal Limits

Liquidity is frequently discussed whenever physical precious metals are mentioned. Gold benefits from broad global recognition and active markets, which is one reason central banks around the world continue to hold substantial gold reserves.

One important point for retirement savers is that physical gold should not be described as instantly liquid or friction-free. That would be inaccurate and inconsistent with how precious metals markets actually operate. Selling physical gold typically involves dealer availability, product verification, market pricing, bid-ask spreads, and standard transaction procedures.

This balanced perspective is important because it helps families set realistic expectations. Gold can often be sold in smaller increments than real estate and may offer more flexibility than certain other tangible assets. However, every transaction remains subject to normal market conditions.

For retirement savers concerned about banking disruptions, the appeal of physical gold is often tied to the fact that ownership is separate from commercial payment systems and institutional account access.

For a detailed discussion of practical selling considerations, see: Liquidity in a Crisis: How to Safely Sell Physical Gold Coins When Banks Implement Withdrawal Limits.

Securing Capital Autonomy Through Tangible Asset Ownership

The purpose of this discussion is not to suggest that banks are unnecessary or that every financial institution faces imminent risk. Banks remain an important part of everyday economic activity. The more relevant question for many retirement savers is whether all family wealth should exist inside the same system.

Bank deposits represent claims within the financial system. Physical gold represents tangible property held outside that system. This distinction is one reason physical precious metals continue to attract attention during periods of inflation concerns, rising debt levels, banking uncertainty, and broader economic instability.

Jefferson Gold’s educational materials consistently emphasize purchasing power preservation, retirement security, and family legacy planning. Physical gold ownership is often discussed within that broader framework rather than as a short-term reaction to market headlines.

For families interested in creating an additional layer of wealth preservation, physical gold ownership may provide structural separation that traditional bank balances cannot offer.

Jefferson Gold helps customers learn about:

- Physical gold and silver purchases

- Direct home delivery options

- Secure vault storage options

- Self-directed precious metals account structures

- Available bullion products

Customers can speak directly with a specialist to discuss available products, delivery procedures, storage arrangements, and account structures.