For many American families, a bank account feels like the safest place for cash. It is familiar, easy to use, and supported by a deposit insurance system that has helped preserve confidence in the U.S. banking system for generations.

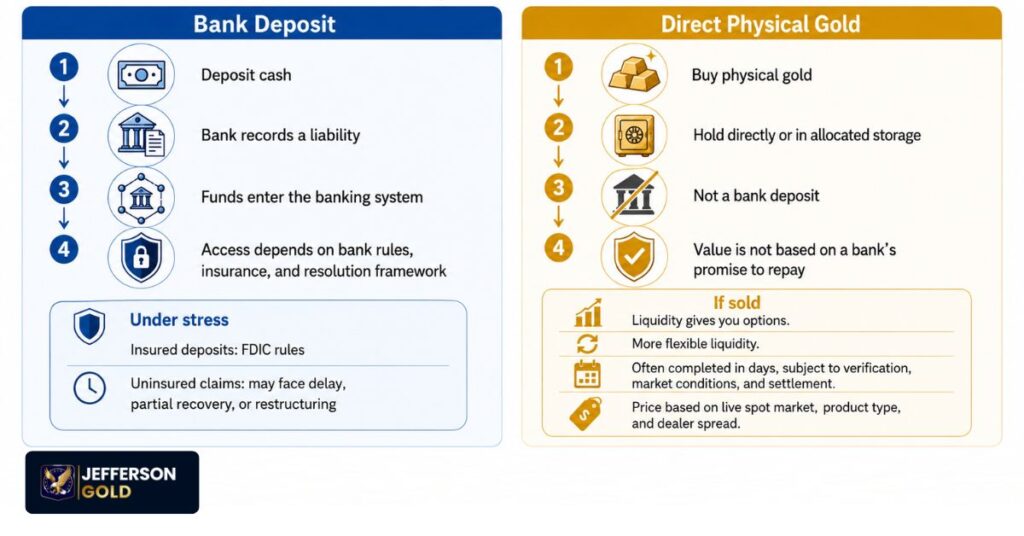

A bank account is not the same as cash in a private vault. Once money enters a commercial bank account, it becomes part of the banking system, and the customer holds a balance the bank must repay under account terms and applicable rules.

That distinction matters during stress. After 2008, U.S. and global regulators created new tools for handling failing large institutions, aiming to reduce panic, protect key functions, and limit taxpayer-funded rescues where possible. For families focused on retirement savings, purchasing power, and legacy planning, these rules are worth understanding.

Understanding how modern banking rules work is only one piece of a broader wealth-preservation strategy. For a deeper look at managing financial uncertainty, read The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

Key Takeaways:

- A bank deposit is not private-vault cash. It is usually recorded as a bank liability.

- FDIC insurance covers eligible deposits up to applicable limits, based on depositor, bank, and ownership category.

- Modern resolution rules may require shareholders and certain creditors to absorb losses before public support is used.

- Dodd-Frank Title II applies to covered financial companies under specific conditions, not as an automatic conversion rule for ordinary insured deposits.

- Physical gold and silver are tangible assets, not bank-account claims, which gives them a different ownership profile.

The Legal Reality of Fiat Custody: Deposits as Unsecured Liabilities

A bank deposit is often described simply: you put money in, and the bank holds it for you. From the customer side, that feels true. But on the banking side, the deposit is recorded as a liability, and the customer receives a right to repayment under account terms, bank rules, and deposit insurance limits.

Not all deposits carry the same risk. FDIC insurance covers eligible deposits at FDIC-insured banks up to the standard limit of $250,000 per depositor, per insured bank, per ownership category. Coverage can vary based on account ownership and structure.

For balances above applicable insurance limits, uninsured funds may be recovered from failed-bank asset sales, but recovery may be partial and may take time. That is the practical difference between insured deposit protection and broader exposure to a failed institution’s balance sheet.

This is why “depositor cash to bank equity” needs careful wording. In the United States, ordinary covered deposits at FDIC-insured banks are protected within applicable limits. The broader concern is that, under certain resolution frameworks, some creditor claims or eligible liabilities can be reduced, restructured, or converted into equity as part of stabilizing a failing institution. 1

Understanding Dodd-Frank Title II and Loss Absorption

Dodd-Frank Title II created the Orderly Liquidation Authority. The FDIC describes this framework as a backstop for resolving certain large, complex financial companies when ordinary bankruptcy may not be possible without serious stability concerns.2

This does not mean ordinary insured checking or savings deposits are automatically converted into bank stock. Institution type, account type, insurance coverage, and the applicable resolution framework all matter.

The larger point is structural: after 2008, resolution policy moved away from relying only on public rescue money and toward models where losses may be absorbed inside the failing institution. In plain English, shareholders, certain creditors, and some liability holders may absorb losses before public funds are used.

The Bank for International Settlements describes modern resolution funding as potentially coming from creditor bail-ins, deposit insurance funds, dedicated resolution funds, and public support as a last resort.3

The Banking Resolution Mechanism: Debt-to-Equity Conversions

A banking resolution mechanism is the process regulators use when a financial institution is failing or close to failing. The goal is to protect critical operations where possible and assign losses according to the legal order of claims.

In a simplified sequence, regulators review the firm’s assets, liabilities, capital position, and systemic importance. Shareholders are usually first in line to absorb losses, followed by certain creditor groups or eligible liabilities, depending on the legal framework.

FDIC insurance separately covers eligible deposits up to $250,000 per depositor, per insured bank, for each ownership category. Balances above applicable limits may be treated differently if a bank fails, depending on account structure and the resolution process. 4

In a debt-to-equity conversion, a claim may be reduced or replaced with ownership shares in a restructured institution. That is the core idea behind “turning cash into bank equity,” though treatment depends on jurisdiction, institution type, account type, insurance coverage, and applicable law.

Historical Case Study: Cyprus and Deposit-to-Equity Conversion

The clearest modern example of deposit-to-equity conversion occurred in Cyprus in 2013. Bank of Cyprus described its recapitalization as a “deposit-to-equity conversion” and stated that 47.5% of eligible bailed-in deposits had been converted to equity.

This does not mean the U.S. system works the same way. Cyprus had its own banking structure, laws, and crisis conditions. But the case shows that, under some resolution systems, balances above protected thresholds can be frozen, reduced, or exchanged for shares in a restructured institution.5

For American families, the lesson is structure, not panic. Wealth held as a bank balance sits inside a financial institution’s balance sheet, while direct physical property has a different risk profile. For more on this comparison, read Physical Gold vs. Bank Bail-Ins (2026 Outlook).

Strategic Asset Insulation Through Physical Gold

Physical gold asset insulation begins with a simple distinction: physical precious metals are tangible property, not a bank’s promise to repay. A bank deposit depends on the institution, insurance structure, and resolution rules that apply during failure.

Physical gold and silver, when directly owned or properly allocated, do not sit on a commercial bank’s balance sheet in the same way. That does not make them risk-free. Prices can rise or fall, and buying, storing, verifying, insuring, shipping, and selling metals all require care.

Physical gold and silver, when directly owned or properly allocated, do not sit on a commercial bank’s balance sheet in the same way. That does not make them risk-free. Prices can rise or fall, and buying, storing, verifying, insuring, shipping, and selling metals all require care.

The ownership structure is different. A gold bar or coin held in direct possession is not a bank liability, not a ledger entry, and not part of a creditor hierarchy inside a failed bank.

That is why some retirement savers and family decision-makers study physical gold and silver as a way to keep part of their wealth outside the banking grid. The goal is to understand where paper claims end and direct ownership begins.

For readers comparing bank-based claims with tangible precious metals, Jefferson Gold’s overview of asset insulation strategies offers a useful next step for learning how physical gold and silver ownership may work in practice.

Implementation Frameworks: Direct Possession and Retirement Accounts

There are two common ways customers study physical precious metals ownership. The first is direct delivery. In this path, a customer buys physical gold or silver and arranges secure delivery. This gives the customer direct possession, subject to personal storage, insurance, and security decisions.

The second is a self-directed precious metals retirement account. This structure may allow certain approved precious metals to be held inside a qualified retirement account through a specialized custodian and approved storage arrangement. Rules can be detailed, and customers should speak with qualified professionals and specialized custodians before making decisions.

For customers comparing physical metals with conventional retirement accounts, Jefferson Gold’s Gold IRA wealth preservation account guide explains the basic structure and key questions to review before getting started.

Physical metals may also be sold through established dealer networks. Sale timing and proceeds can vary based on product type, dealer availability, authentication, market hours, bid-ask spreads, shipping, storage arrangement, and settlement method. Gold is widely recognized, but liquidation should never be described as instant, cost-free, or guaranteed.

Protecting Long-Term Retirement Capital from Systemic Failure

To protect retirement from bank failure, it helps to understand what different assets actually are. A checking account is a claim on a bank, protected within applicable FDIC limits at insured institutions.

Brokerage accounts, retirement accounts, annuities, real estate deeds, gold coins, and private vault accounts all carry different rules, risks, and ownership structures. Treating them as identical can create blind spots.

Modern bank bail-in laws were designed to manage institutional failure without automatically placing every loss on taxpayers. That makes creditor hierarchy, deposit insurance, and account structure especially important for families with meaningful savings.

Physical gold and silver offer a different form of ownership: tangible assets that can exist outside a commercial bank’s balance sheet. For families focused on purchasing power, inheritance, and long-term wealth preservation, that difference is worth understanding.