Many families think of a bank balance as cash sitting safely in their name. In daily life, that is how it feels. You log in, see the number, pay bills, and assume the money is fully available. The Bank Recovery and Resolution Directive raises a more serious savings-risk question: what happens when the bank itself becomes the problem?

The BRRD is an EU framework for handling troubled banks. U.S. readers should not treat it as directly applicable American law, but it is useful for understanding how post-2008 resolution thinking has changed. For American families focused on retirement savings and family wealth preservation, the goal is not fear.

The goal is to know the difference between insured deposits, uninsured balances, bank claims, and physical assets held outside the banking network.

This topic connects upward to The Ultimate Guide to Protecting Your Wealth in a Volatile Economy, which gives broader context for families reviewing banking, inflation, debt, and hard-asset exposure.

Key Takeaways:

- BRRD rules apply when a bank is failing, not during normal everyday banking.

- A bail-in uses the bank’s internal capital structure, while a bail-out uses public money.

- FDIC insurance generally protects up to $250,000 per depositor, per insured bank, per ownership category in the U.S.

- Uninsured balances may carry more risk during a bank resolution, depending on account type, ownership structure, insurance limits, and applicable legal framework.

- Physical gold held outside the banking system is not a bank liability, so it is structurally separate from bank bail-in tools.

The Structural Shift from Taxpayer Bail-Outs to Institutional Bail-Ins

After the 2008 financial crisis, governments and regulators faced a political problem. Public bail-outs helped keep major institutions from failing in a disorderly way, but taxpayers were left asking why private banking losses had become a public burden. 1

Modern resolution rules were built to reduce that burden. Under a bail-in model, losses are first absorbed inside the failing institution. Shareholders usually take losses first, followed by certain debt holders and other unsecured claims, depending on the legal structure and the specific resolution plan.

This is the core of bank bail-in vs bail-out mechanics. A bail-out reaches outward to taxpayers. A bail-in reaches inward to the bank’s own capital structure. The Financial Stability Board’s Key Attributes set an international standard for resolution regimes designed to resolve systemically important institutions without taxpayer exposure to solvency losses, while keeping vital functions running. 2

In the United States, Title II of the Dodd-Frank Act gives the FDIC Orderly Liquidation Authority for certain large, complex financial companies when their failure could threaten system stability. This is not the same as saying ordinary insured bank deposits are automatically converted under Title II. Institution type, account type, insurance coverage, and the resolution framework all matter. 3

The Legal Reality of Modern Bank Deposits: Your Status as an Unsecured Creditor

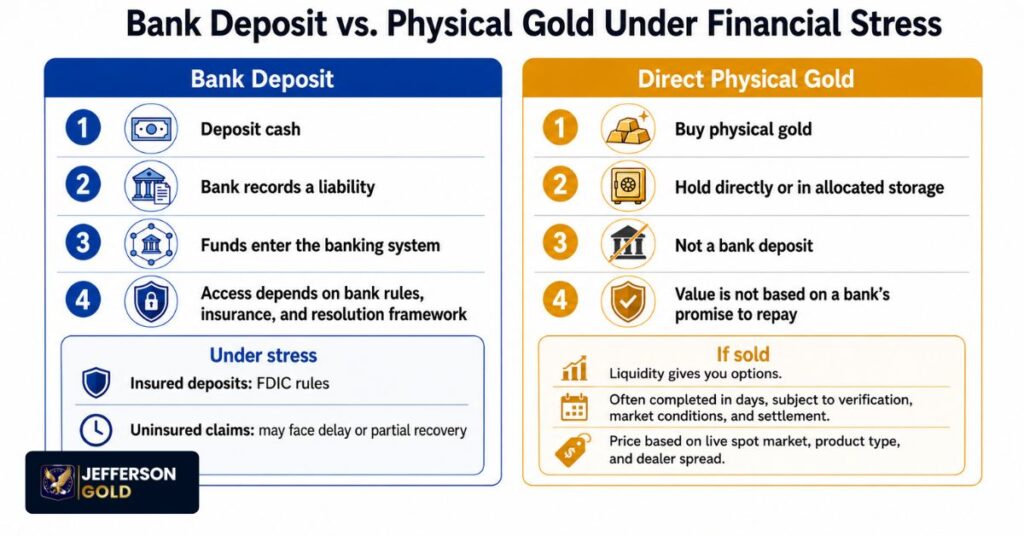

A bank deposit is not usually a separate envelope of cash with your name on it in the vault. In general terms, the bank owes you the balance shown in your account, and deposit insurance protects eligible deposits up to applicable limits. That makes insured coverage important, especially for families holding large cash balances.

In the United States, the standard FDIC insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. The FDIC adds together accounts in the same ownership category at the same insured bank when calculating coverage. 4

Balances above insured limits can carry different risk than insured deposits. That does not mean an uninsured balance is automatically lost in a bank failure. It means the account holder should know what is insured, what is not, and how the rules may apply if a bank enters resolution.

Statutory Bail-In Depositor Status: Where Uninsured Balances May Sit

During a bank resolution, not every claim is treated the same way. Losses are generally applied in a hierarchy, starting with the parties that accepted the most risk. For families, the important point is that insured deposits and uninsured balances may not sit in the same protection category. The table below gives a simplified view of where different claims may fall.

| Category | Typical Role in a Bank Failure | Practical Meaning for Families |

| Shareholders | Usually Absorb Losses First | Equity Can Be Reduced or Wiped Out |

| Subordinated Debt Holders | Usually Next in Line | Claims May Be Reduced or Converted |

| Senior Unsecured Debt Holders | May Be Affected After Lower Tiers | Treatment Depends on the Resolution Plan |

| Certain Uninsured Claims | May Face Risk in Some Systems | Treatment Depends on Limits, Law, And Account Type |

| Insured Deposits | Protected Up to Statutory Limits | Coverage Depends on Ownership Category and Local Rules |

The table is simplified. Real-world bank resolution depends on the institution type, account structure, insurance limits, applicable legal framework, and the authority managing the process.

Understanding the Mechanics of the Statutory Write-Down and Conversion Tool

Under the BRRD, the bail-in tool can write down debt owed by a bank to creditors or convert it into equity. The Single Resolution Board describes bail-in as a key resolution tool within the Banking Union.

A simplified loss sequence may look like this:

- Shareholders generally take losses first.

- Certain subordinated debt may be reduced or converted.

- Senior unsecured debt may be affected after lower tiers.

- Certain uninsured claims may be reviewed, depending on account type, insurance limits, and the applicable resolution framework.

The point for families is simple: money inside a bank depends on that bank’s systems, solvency, and legal framework. In a severe failure, access and treatment may depend on rules the account holder does not control.

Protection against bank bail-ins starts with knowing which balances are insured, which are uninsured, and which parts of family wealth sit outside bank resolution rules entirely.

Comparative Analysis: Historical Precedents of Depositor Capital Restructuring

Cyprus remains the most cited modern example of depositor capital restructuring. In 2013, Cyprus restructured Laiki Bank and Bank of Cyprus during the Eurozone debt crisis. Insured deposits up to €100,000 were protected, while uninsured Bank of Cyprus deposits above €100,000 were partly converted into equity. 5

Bank of Cyprus later reported that 47.5% of uninsured deposits were converted into equity as part of the recapitalization. This confirms the figure often cited in public discussions of the Cyprus bail-in.

Cyprus was not the United States, and it was not a normal bank failure. But it showed that, under severe conditions, uninsured deposits can become part of a bank restructuring plan. 6

That distinction matters. The lesson is not that all banking systems work the same way. For U.S. account holders, the relevant questions are how FDIC insurance limits apply, how accounts are titled, and how insured and uninsured balances may be treated if an institution fails.

Counterparty Risk Protection: Strategic Asset Insulation Through Physical Precious Metals

A bank account depends on a bank. A digital balance depends on account access, payment systems, compliance systems, and the institution’s ability to operate. Physical gold held directly outside the banking system has a different structure. It is not another party’s promise to pay.

The World Gold Council describes gold as a highly liquid asset that is no one’s liability and carries no credit risk. That does not mean gold is risk-free. Prices move, dealer spreads exist, and selling physical metals depends on product type, authentication, market hours, dealer availability, storage method, and settlement process. 7

This is why many families review physical gold as a physical gold banking risk hedge. Physical gold held directly is not a bank deposit and is not converted into bank stock because a bank enters resolution. The risk profile is different from a bank account because the asset does not sit on the bank’s balance sheet.

Jefferson Gold helps customers learn about physical gold and silver, compare available products, review pricing, and understand delivery or storage choices. Readers can also review Jefferson Gold’s asset insulation strategies page for more educational context.

Some customers prefer direct home delivery. Others want secure storage information. Some retirement savers ask about self-directed account structures, which should be reviewed with qualified custodians and personal professionals before any decision is made.

Conclusion: Protecting Your Financial Legacy Outside Bank Resolution Risk

The Bank Recovery and Resolution Directive represents a post-2008 change in how regulators think about failing banks. The older model leaned heavily on taxpayer bail-outs. The newer model asks the institution’s own capital structure to absorb losses first.

For families, the main lesson is clear: know what you own, where it sits, what protects it, and what rules apply if the institution holding it comes under stress. Bank deposits still serve an important role. Deposit insurance matters. But insured deposits, uninsured balances, paper claims, and directly held physical assets are not the same thing.

Physical gold and silver offer a different structure. They are tangible. They are not bank liabilities. They are not dependent on a failing institution’s recapitalization plan. For retirement savers focused on family wealth preservation, that difference may be worth a serious conversation.

Have questions about buying physical gold or silver? Speak with a Jefferson Gold specialist to learn more about available products, pricing, delivery, and storage options.