Modern banking depends on confidence. Most of the time, paychecks clear, wires move, cards work, and ATMs dispense cash. During a banking shock, transfers may slow, branch access may narrow, and large withdrawals may require advance notice.

That does not mean every bank balance is unsafe. In the United States, FDIC coverage generally protects up to $250,000 per depositor, per insured bank, per ownership category. The practical issue is access: protection and immediate availability are not always the same during a high-stress event.1

That is why many families and retirement savers consider physical gold coins as part of a wealth preservation plan. Physical coins are tangible assets, not bank deposits, and they do not require an online login, wire window, or local branch to exist.

For a broader view of crisis planning, see The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

Key Takeaways:

- Physical gold coins may give owners another path to liquidity when bank withdrawal limits, transfer delays, or local branch disruptions make cash access more difficult.

- Recognized sovereign coins are often easier for qualified dealers to review because their weight, purity, markings, and mint origin are widely known.

- Selling physical gold during a crisis still requires planning. Dealer availability, product verification, shipping, settlement method, market hours, and bid-ask spreads can all affect timing and final proceeds.

Understanding Capital Controls and the Anatomy of an Institutional Banking Freeze

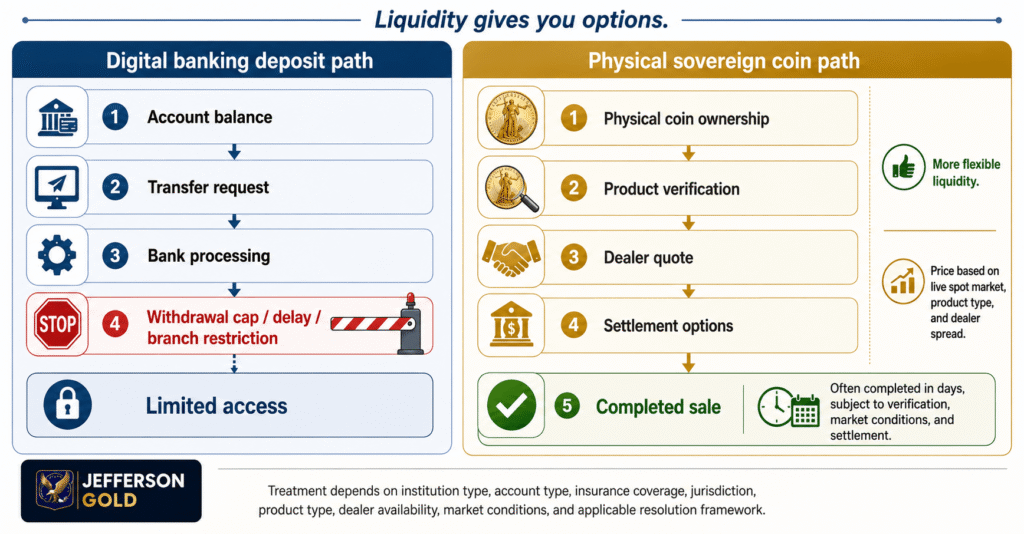

A bank withdrawal limit caps how much an account holder can remove or transfer within a set period. Capital controls are broader government or central-bank limits on moving money out of a banking system, currency zone, or country.

These measures are usually presented as temporary crisis tools to slow bank runs and preserve liquidity. For households, the issue is access: money may still be in the bank, but restricted withdrawal windows can make it harder to use when needed.

The United States has separate rules for deposit insurance, bank receivership, and large-company resolution under frameworks like Dodd-Frank Title II. These should not be treated as the same thing or reduced to claims that ordinary insured deposits are automatically converted during every bank failure.

Still, banking stress can create practical problems: failed wires, blocked transfers, cash shortages, branch closures, and uncertainty around uninsured balances. That is one reason physical ownership matters to many gold buyers. For more on this cluster topic, read Physical Gold vs. Bank Bail-Ins (2026 Outlook).

Verifying Sovereign Bullion Attributes to Ensure Immediate Market Acceptance

If the goal is to safely sell physical gold coins in a crisis, the first step happens before the crisis: know exactly what you own. Dealers typically review country of issue, mint origin, year, denomination, weight, purity, condition, packaging, documentation, and signs of tampering or counterfeit risk.

Sovereign bullion coins can be easier to review than unfamiliar private products because their specifications are public and widely recognized. American Eagle Gold Bullion Coins, for example, are listed by the U.S. Mint with a 91.67% gold composition, with silver and copper making up the balance.2

More broadly, recognized sovereign coins often have known weights, designs, purity profiles, and mint origins, which can help a dealer confirm what the coin is before pricing it. Still, the dealer may need to inspect the coin, confirm authenticity, and apply the firm’s current buy price before completing a sale.

This does not mean every sovereign coin sells at the same speed or same spread. A dealer may still need to inspect the coin, confirm authenticity, check market conditions, and apply the firm’s current buy price. Before a sale, owners should organize coins by type, keep purchase records where available, avoid cleaning or altering coins, and store them in a way that protects condition.

Executing Physical Settlement: Private Dealer Networks and Counterparty Mitigation

Selling physical gold coins during a stressful period should begin with a clear process. Contact a qualified precious metals dealer before transporting anything, and ask what they are buying, how they verify coins, how pricing is set, and which settlement methods are available.

Request a live quote that explains the spot reference, the dealer’s buy price, and any spread or fee. In fast-moving markets, quotes may expire quickly as prices, demand, and inventory change.

Confirm settlement before completing the sale. Payment may involve wire, check, ACH, vault transfer, account credit, or another approved method, but options may be narrower if local banking networks are restricted.

Plan transportation carefully. Avoid informal meetups, do not advertise what you are carrying, and use insured, trackable, dealer-approved shipping or logistics when appropriate.

Keep records of what was sold, when it was sold, how it was valued, and how settlement was handled. Jefferson Gold can help customers understand available products, physical gold coin delivery options, pricing, and storage-related questions. For current buy and sell information, contact us for a real-time quote.

Managing Liquidation Velocity and Navigating Transactional Friction

Liquidity is not the same thing as instant cash. Gold is widely traded around the world. The World Gold Council describes gold as a liquid asset and tracks trading across OTC, futures, and ETF markets. That broad market activity helps explain why recognized gold products often have strong resale demand.

A household selling physical coins still faces real steps. A dealer must verify the product. The parties must agree on a bid. Settlement must clear. If the coins are stored offsite, a vault may need transfer instructions. If the owner holds coins personally, secure delivery may need to be arranged.

During a banking freeze, these steps can become slower, not faster. Demand may rise. Spreads may widen. Dealer inventory may tighten. Shipping networks may face delays. Some buyers may pay more for recognized coins, while others may pause until markets settle.

A safer expectation is this: sovereign coins may provide more flexible liquidity paths than many larger, less divisible assets, but the sale process is still subject to verification, pricing, logistics, and lawful reporting rules.

Historical Analysis of Physical Liquidations During Systemic Asset Freezes

A useful modern case study is Cyprus in 2013. According to IMF materials, Cyprus faced a banking crisis that included a six-day bank holiday, temporary capital controls, and deposit withdrawal restrictions when banks reopened in March 2013. 3

IMF research on crisis-driven capital controls also notes that Cyprus introduced controls in the context of a major bail-in of deposits at the two largest banks. The lesson is not that the same event will happen in the United States or Canada. The systems, laws, and banking structures are different.

The lesson is that modern banking systems can restrict access during a crisis, even in developed economies. When controls are imposed, the household problem is not only account value. It is access. Can money move? Can a bill be paid? Can a family respond? 5

Physical gold coins do not remove every risk. Prices can move. Premiums can change. Dealers may require verification. Settlement options may depend on the banking environment. But coins held outside the banking system may give owners more than one path to value when one path is blocked.

Prioritizing Personal Asset Insulation Ahead of Volatile Macroeconomic Shifts

The best time to plan a liquidation path is before a banking emergency, not during one. That means knowing what you own, where it is stored, which dealer you would call, how that dealer verifies products, what settlement methods may be available, and what records you need to keep.

Storage deserves careful thought. Home placement may offer immediate personal access, but it also creates security concerns. Professional storage may provide insured vaulting and formal records, but access depends on the storage agreement, hours, and procedures. Neither path is perfect for every family.

The goal is not to predict the next crisis. The goal is to avoid having every option depend on a single bank login, a single branch, or a single transfer network. Physical gold coins may play a role in asset insulation strategies because they are tangible, widely recognized, and not issued as a liability of a commercial bank.

Jefferson Gold helps customers learn about physical gold and silver, direct ownership, available storage information, and liquidation paths. A short planning conversation before stress hits can be far more useful than a rushed call during a bank holiday.