Families often think about what they own, but they may spend less time thinking about where it is held. That location can matter during periods of banking stress, political uncertainty, or market disruption.

If every account, asset, document, and emergency reserve sits inside one country, one banking system, or one local legal process, that creates a single point of failure. Geographic separation is designed to reduce that concentration.

Jurisdiction diversification gold planning does not mean abandoning domestic holdings. It means asking a practical question: should every physical asset remain under the same local rules, local access points, and local financial controls?

This is where physical gold differs from many paper-based holdings. Properly held bullion can be stored outside the banking system, outside a local safe deposit box, and outside a single domestic access point.

Key Takeaways:

Jurisdiction diversification gold planning means storing some physical precious metals outside the owner’s home legal system, often in a private international vault. The goal is to avoid keeping every form of physical wealth under one local banking or regulatory system.

For U.S. buyers in Florida, Texas, California, the Midwest, and beyond, private international vault storage may support wealth preservation planning, but it depends on vault quality, ownership records, insurance, reporting duties, and sale procedures. It should be reviewed with qualified professionals, not treated as a one-size-fits-all answer.

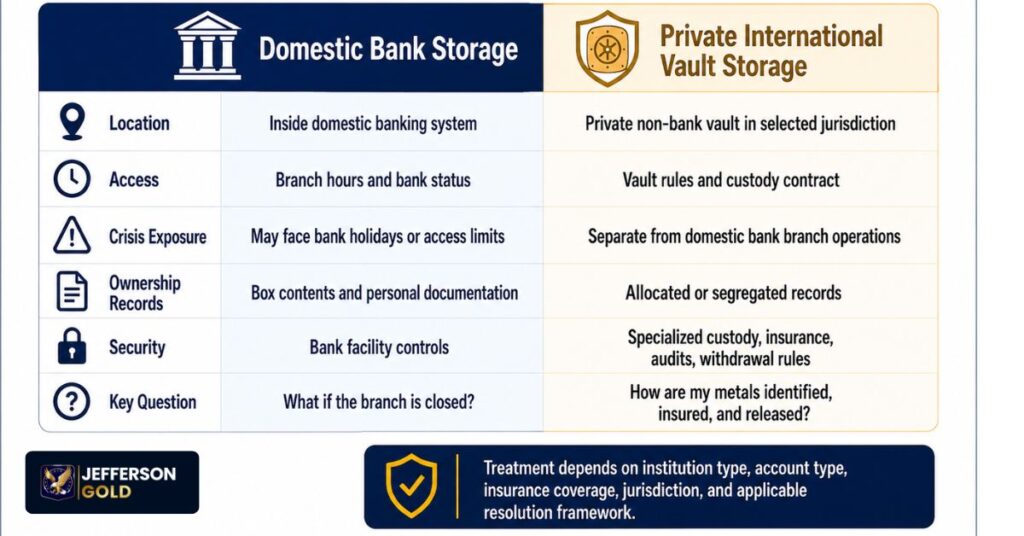

The Vulnerability of Domestic Custody in a Shifting Economic Landscape

Domestic custody is familiar. It can also be concentrated. A local bank account, a bank safety deposit box, and domestic financial paperwork may all depend on the same operating system: open branches, active payment rails, working courts, functioning banks, and normal access rules.

This does not mean bank deposits are unprotected. In the United States, FDIC deposit insurance generally covers up to $250,000 per depositor, per insured bank, for each ownership category.1 That protection is meaningful, but deposit insurance is not the same thing as physical custody of a specific gold bar or coin in a non-bank vault.

Modern bank resolution rules should be discussed carefully. In the U.S., Dodd-Frank Title II applies to large, complex financial companies; it is not a blanket rule that ordinary insured deposits are automatically converted in every bank failure. The key point is simpler: bank-based claims and physical, allocated precious metals are different forms of ownership.

Capital controls can also affect access during financial stress. IMF materials explain that capital flow management measures may be used in certain circumstances, including when capital flows create macroeconomic or financial stability risks.2 For families, the lesson is not panic. It is preparation.

Strategic Geographies: Identifying Secure International Vault Destinations

Offshore gold vault storage is only as strong as the country, facility, contract, and custody process behind it. A stable vault destination should be reviewed through practical questions: does the country have political stability, strong private property protections, a predictable legal system, and a respected vaulting industry?

Commonly discussed storage hubs include Switzerland, Singapore, and New Zealand. These locations are often reviewed because of their reputations for political stability, property protections, strong logistics, and distance from U.S.-only banking infrastructure. A buyer should still review the exact facility, agreement, insurance, and access rules before making any decision.

Evaluating Political Neutrality and Statutory Protections

A strong offshore destination is not chosen because it sounds distant or exclusive. It is chosen because the legal and operating environment is stable, predictable, documented, and resistant to sudden interference.

For precious metals, a buyer should ask whether the vault operates as a private non-bank depository, whether it has clear inventory records, whether the metals are allocated or segregated, and whether the facility provides independent audit reporting.

The London Bullion Market Association’s Good Delivery framework is useful context when discussing recognized wholesale gold and silver standards. LBMA Good Delivery Rules cover specification standards for London-traded gold and silver bars, and LBMA’s Good Delivery List is used globally as a reference point for recognized refiners and market confidence. 3 4

Private Non-Bank Depositories vs. Traditional Financial Institutions

A bank safety deposit box and a private non-bank vault are not the same thing. A bank safety deposit box is inside a bank facility. Access can depend on branch hours, local banking rules, and whether the bank is open during a crisis.

A private non-bank depository is built for physical custody. Stronger facilities focus on metals intake, verification, insurance, inventory reporting, segregated or allocated storage, withdrawal procedures, and audited controls.

That difference matters. The goal is not to claim that every bank facility is unsafe or that every private vault is perfect. The goal is to separate two different types of custody: bank-adjacent storage and independent physical storage.

For buyers who want to learn more about delivery and purchase paths, Jefferson Gold can explain the physical gold and silver purchase process.

Historical Precedent: The Mechanics of Systemic Wealth Insulation

History shows why location matters. During the 2013 Cyprus banking crisis, uninsured deposits at certain banks were affected as part of the restructuring process, showing how local banking stress can quickly become an access problem for account holders. 5

The Cyprus case does not directly map onto the U.S. system, which has its own deposit insurance rules and bank resolution process. The broader lesson is that assets held inside a stressed local banking structure may be subject to rules the account holder does not control.

Physical gold held in a private, insured, non-bank vault in a stable jurisdiction may sit outside that local bank balance-sheet issue. Still, custody terms, vault provider, title records, account structure, reporting duties, and sale procedures should all be reviewed first.

For families considering international vault storage, the goal is not guaranteed protection from every risk. It is to understand how location, custody structure, and physical ownership may support long-term wealth preservation.

Systemic Interconnectedness: Capital Insulation and Downward Risks

Domestic bank risk, capital movement limits, and physical custody choices are connected. Families do not need to predict the next crisis to see that keeping everything under one system can create exposure.

Jurisdiction diversification focuses on where physical gold is held, how it is stored, and whether the custody structure sits inside or outside the banking system. This creates a bridge to future content on stable international vault selection, custody documentation, and offshore storage procedures.

Bank recovery rules, such as Europe’s BRRD, should be discussed as case studies, not broad claims about every country or account. Readers who want the regulatory background can continue with What the Bank Recovery and Resolution Directive Means for Your Savings.

Depositor treatment during bank stress should also be handled with careful boundaries. Deposit accounts, insured coverage, uninsured balances, and bank resolution rules are different from holding specific physical metals in a private vault. A related guide, How Modern Banking Laws Turn Depositor Cash Into Bank Equity, explains that issue in more detail.

Gold liquidity in a crisis deserves its own careful discussion. Gold has a deep global market, but selling coins or bars is not instant in every case. Dealer availability, product type, authentication, market hours, shipping, vault procedures, settlement method, and bid-ask spreads can all affect timing and price.

For a practical selling-focused article, see Liquidity in a Crisis: How to Safely Sell Physical Gold Coins When Banks Implement Withdrawal Limits.

Legal and Operational Logistics of Asset Migration

Moving precious metals offshore is an operational process, not a slogan. A careful process usually includes confirming the buyer’s goals, selecting the vault jurisdiction, confirming allocated or segregated storage terms, documenting product details, arranging insured transport, receiving vault confirmation, and keeping ongoing statements and audit records.

Segregated storage is often the stronger custody model for buyers who want clear item-level tracking. Allocated storage can also identify metal held for the customer, but the exact meaning can vary by provider. Buyers should ask for written explanations before choosing a storage path.

U.S. persons should also review reporting requirements with qualified professionals. The IRS explains that certain foreign financial accounts may need to be reported through FBAR using FinCEN Form 114, and FinCEN states that U.S. persons with a financial interest in or signature authority over foreign financial accounts must file when the aggregate value exceeds the reporting threshold.5 6

Whether a particular precious metals custody arrangement triggers reporting can depend on the structure, so buyers should not guess.

Conclusion: Securing the Cross-Generational Anchor

For families focused on long-term wealth preservation, jurisdiction diversification is about reducing dependence on one system. It is not about fear. It is about structure. Domestic storage may be convenient. Offshore private vaulting may add distance from local banking disruptions.

Physical gold may offer a tangible form of wealth outside many paper-based systems. But each choice has tradeoffs, including cost, access rules, reporting duties, transport procedures, and sale timelines.

The strongest approach begins with questions: Where is the asset held? Who controls access? Is it inside a bank or outside one? Is the metal allocated or segregated? How is it audited? What happens during a banking closure? What records will the family have?

Jefferson Gold helps customers learn about physical gold, direct delivery, and storage-related paths so they can better understand how tangible assets may fit into broader asset insulation strategies. For questions about products, pricing, delivery, and storage, speak with a Jefferson Gold specialist.