For many American families, the Federal Reserve feels like a domestic institution. It sets interest rates, manages liquidity conditions, and influences borrowing costs across the United States economy. However, the Federal Reserve monetary policy gold relationship extends far beyond domestic borders.

When U.S. interest rates remain elevated, the dollar can strengthen and global financial conditions can tighten. Emerging economies that rely heavily on external dollar funding may then face greater pressure on currencies, capital flows, and reserve management.

This environment can help explain why some emerging-market central banks review the role of gold within broader reserve-diversification strategies. Gold purchases are not determined by Federal Reserve policy alone, however. Decisions also reflect domestic conditions, geopolitical risk, reserve composition, market valuation, and long-term institutional priorities.

Key Takeaways:

- During restrictive Federal Reserve policy cycles, elevated U.S. interest rates can strengthen the dollar and tighten global financial conditions, influencing capital flows and adding currency pressure in some emerging economies.

- Research from institutions such as the World Bank shows that U.S. rate increases can raise local bond yields, widen sovereign spreads, weaken currencies, and reduce capital inflows in developing economies.

- The 2025–2026 reserve composition shift reflects both valuation effects and diversification trends, with gold representing a significantly larger share of official reserves compared with previous decades, according to multi-year central bank datasets.

- The 2026 World Gold Council survey indicates that a large majority of central banks expect higher gold reserve levels globally, while many also expect a declining share of the U.S. dollar in global reserves over the medium term.

- Central-bank gold demand remains structurally elevated compared with long-term historical averages, even when annual flows fluctuate across cycles.

The Federal Reserve Transmission Mechanism and Global Currency Strains

Federal Reserve monetary transmission describes how U.S. interest rate decisions, liquidity conditions, and dollar strength influence global financial systems. When U.S. rates remain elevated, global investors tend to shift toward dollar-denominated assets due to higher relative yields and perceived safety.

This can reduce available financing and increase pressure on economies that depend heavily on external funding. Over time, this mechanism affects sovereign balance sheets, foreign exchange reserves, and domestic monetary stability across developing economies.

Dollar Strength, Capital Flow Reallocation, and Emerging Market Pressure

When U.S. interest rates remain above global averages, capital flows reallocate toward dollar assets due to yield advantage and lower perceived risk. This can reduce available financing in emerging markets and increase pressure on local currencies. As currencies weaken, governments face higher external debt servicing costs in domestic terms and reduced monetary flexibility.

In some circumstances, capital outflows and currency depreciation can reinforce one another, particularly where external debt levels, reserve buffers, and market confidence are under strain.

Import Pricing, Inflation Channels, and Fiat Devaluation Effects

When local currencies weaken against the dollar, the domestic cost of dollar-priced imports can rise. This may add to inflation pressure, especially in economies that depend heavily on imported energy, food, industrial inputs, or external financing. The scale of the effect varies by country, exchange-rate regime, and domestic policy response.

Why Bullion Becomes Part of the Reserve Response

Emerging-market central banks adjust reserve composition when paper-based assets become more sensitive to global monetary cycles, liquidity constraints, and currency volatility. Physical bullion functions differently from traditional reserve assets because it is not issued as a liability by any single government or financial institution. This structural independence allows bullion to function as a neutral reserve component during periods of monetary stress and policy uncertainty.

Structural Reserve Adjustment and Institutional Risk Management

Central-bank gold decisions are generally shaped by longer-term reserve objectives, though timing and purchasing patterns can vary with market conditions and country-specific needs. During periods of greater monetary or geopolitical uncertainty, some reserve managers may reassess their exposure to foreign-issued debt, currencies, and other financial claims.

Physical bullion is therefore used as a non-liability reserve component that reduces dependency on any single sovereign issuer, payment system, or financial intermediary network.

Monetary Transmission Effects and Bullion Allocation Behavior

Elevated U.S. interest rates influence bullion demand through interconnected macro channels. Stronger dollar conditions increase external funding pressure, tighter global liquidity reduces financial flexibility, and currency depreciation raises the cost of maintaining reserves.

These combined pressures may encourage some reserve managers to reassess the balance between currencies, sovereign debt, and gold, but the timing and scale of any change varies widely by country.

For a broader overview of how physical metals may fit into long-term wealth preservation during economic uncertainty, learn more about Jefferson Gold’s approach to wealth preservation through gold.

Emerging Market Central Banks Bullion Accumulation Dynamics

Global central banks have increased gold allocations over the past decade due to reserve diversification needs, geopolitical risk considerations, and valuation effects. While gold now represents a larger share of global reserves than in previous cycles, this shift is driven by both active accumulation and rising market valuation rather than uniform liquidation of traditional reserve assets such as sovereign debt instruments.

Reserve Composition Changes and Valuation Effects

Gold’s share of global reserves has increased in part because central banks have added to holdings and in part because higher gold prices have raised the market value of existing reserves. The European Central Bank reported that gold became the second-largest global reserve asset at market prices in 2024, after the U.S. dollar. That does not mean gold displaced U.S. Treasuries as the dominant reserve instrument or that central banks were uniformly selling government debt to buy bullion.

Central Bank Demand Trends and Structural Allocation Patterns

Central bank gold demand remains elevated relative to long-term historical averages. While annual flows vary depending on monetary cycles and geopolitical conditions, multi-year datasets show persistent allocation interest. This indicates that gold is increasingly treated as a structural reserve component within sovereign balance sheets rather than a temporary defensive allocation response to short-term volatility.

Sovereign Accumulation Case Examples

Countries such as Poland and the People’s Bank of China (PBoC) demonstrate different accumulation strategies.

- Poland has continued to add to its reported gold reserves. In Q1 2026, the National Bank of Poland increased holdings by 31 tonnes to 582 tonnes. 1

- The People’s Bank of China has also reported continued additions to its gold reserves over recent years. 2

For a macroeconomic framework on systemic financial risk and long-term preservation strategy, see The Ultimate Guide to Protecting Your Wealth in a Volatile Economy.

De-Dollarization and the Multipolar Reserve Landscape

De-dollarization refers to gradual diversification away from single-currency dependency in global reserves and trade settlement systems. It does not imply replacement of the U.S. dollar but rather expansion of alternative settlement mechanisms and reserve assets designed to reduce reliance on a single financial infrastructure.

This represents structural diversification of global monetary architecture rather than a direct currency replacement system.

BRICS Structure and Currency Misconceptions

BRICS does not operate a unified currency system and should not be interpreted as a direct alternative to the U.S. dollar. Instead, it functions as a coordination framework among emerging economies focused on trade alignment, financial cooperation, and settlement diversification. Therefore, BRICS should be understood as a geopolitical and economic coordination mechanism rather than a monetary union or currency replacement bloc.

SWIFT Exclusion and Reserve Access Risk

SWIFT exclusion refers to restricted access to global banking communication systems used for international settlement messaging. While distinct from direct asset freezes, it increases systemic awareness of financial access vulnerability during geopolitical stress.

Events in 2022 demonstrated that sovereign reserves can become partially inaccessible under extreme conditions, which has influenced long-term reserve allocation and diversification strategies.

Family Protection Frameworks Mirroring Sovereign Asset Insulation

Households and central banks operate at different scales but share exposure to paper-based financial systems. Families increasingly study sovereign reserve behavior to understand structural differences between financial claims and physical assets, particularly in terms of custody structure, counterparty exposure, and long-term purchasing power stability across economic cycles.

Paper-Based Financial Claims Versus Physical Custody Structures

Traditional financial assets such as bank deposits, bonds, and retirement accounts represent contractual claims within financial systems rather than direct ownership of physical assets.

These instruments depend on institutions, legal frameworks, and counterparties. Physical bullion can differ from financial claims because allocated or directly held metal may not depend on an issuer’s repayment promise. The level of ownership, custody control, and counterparty exposure depends on the specific purchase and storage arrangement.

Ownership Pathways and Retirement Structure Considerations

There are two primary educational pathways for physical metal ownership. The first is direct physical delivery, where individuals take custody of metals and manage storage independently.

The second is participation in self-directed retirement structures that may hold IRS-eligible precious metals under regulated custodial arrangements. Each pathway involves different storage, access, and compliance requirements that must be evaluated within appropriate financial and legal frameworks.

Readers considering retirement-account structures can learn more about pursuing a secure retirement with precious metals through Jefferson Gold’s Gold IRA 101 resource.

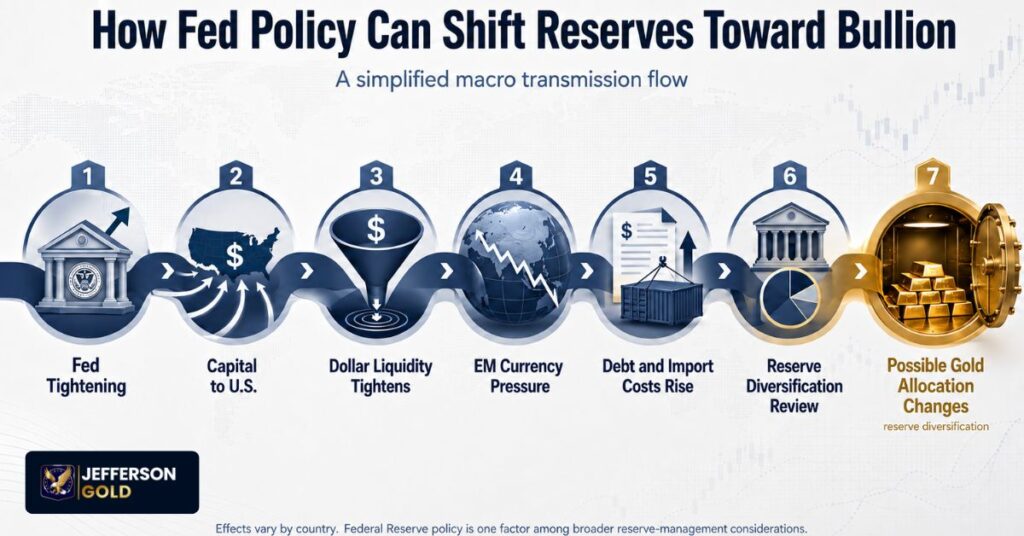

How These Forces Interact Across the Global Monetary System

The full transmission model linking Federal Reserve policy to global reserve behavior can be understood as a connected sequence of pressures rather than a single cause.

When U.S. monetary policy becomes restrictive, global capital flows tend to shift toward dollar assets. This reduces liquidity in emerging markets and increases funding pressure across sovereign and corporate balance sheets. Currency depreciation follows, which raises import costs and external debt burdens.

As these pressures accumulate, central banks reassess reserve structures, often placing greater emphasis on diversification and non-liability assets such as physical bullion. This adjustment is typically gradual and varies by country, but it reflects long-term risk management rather than short-term reaction.