Inflation protection with gold has become an important topic for many families in the United States and Canada as rising prices continue to affect purchasing power. While inflation rates change over time, the long-term concern is whether savings can maintain their real-world buying power.

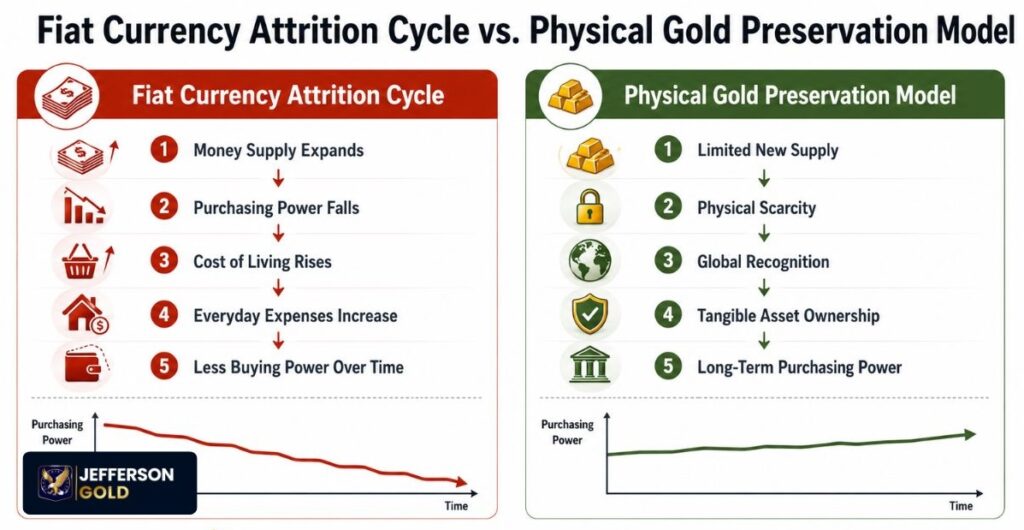

Physical gold differs from fiat currency because its supply cannot be expanded through monetary policy decisions. New gold production requires mining, refining, specialized labor, equipment, and substantial operating capital, which naturally limits supply growth.

For families concerned about inflation, debt expansion, and long-term purchasing power, physical gold continues to be studied as a tangible asset with a long history of preserving purchasing power.

This article is part of Jefferson Gold’s broader guide to protecting wealth in a volatile economy, which examines how tangible assets, purchasing power, liquidity, and account structures interact during periods of monetary stress.

Key Takeaways:

- Physical gold is limited by geology, mining costs, refining capacity, and time. Paper and digital currency units can be expanded by policy.

- Inflation reduces purchasing power when more currency chases the same amount of goods, services, and scarce assets.

- Direct physical gold ownership can reduce dependence on paper promises, third-party issuers, and account-based systems.

- Certain precious metals may be held in specialized self-directed retirement accounts when strict product, custody, and storage rules are met. Customers should speak with qualified custodians and professionals before making account decisions.

The Mechanics of Currency Expansion and Purchasing Power Attrition

Currency debasement begins with a simple relationship: when the supply of money rises faster than the supply of goods and services, more currency units compete for the same real goods. The Federal Reserve describes seasonally adjusted M2 as M1 plus small-denomination time deposits and retail money market funds.

FRED’s M2 series shows that U.S. broad money supply remains substantially above its pre-2020 level. This is one reason finance publishers and macro analysts continue to discuss the relationship between money supply growth, inflation pressure, and hard assets. 1

CPI is useful, but it is not the same as every household’s personal cost of living. BLS states that CPI measures the average change over time in prices paid by urban consumers for a market basket of goods and services.

Gold responds to this problem from the opposite direction. It cannot be printed, digitally expanded, or created through a policy vote; above-ground supply changes slowly because mine output is physically constrained.

How Purchasing Power Changes Over Time

Inflation is often discussed as a percentage, but families experience it through everyday expenses. A dollar that purchased a larger basket of groceries years ago may purchase fewer items today. The same principle applies to housing, healthcare, transportation, insurance, and other necessities.

The challenge for retirement savers is that purchasing power erosion frequently occurs while account balances remain unchanged. A savings balance may show the same number, yet the real-world buying power behind that balance can decline as prices rise.

This distinction between nominal value and purchasing power sits at the center of discussions about inflation protection with gold. The question is not simply how many dollars an asset is worth. The more important question is how many goods, services, and necessities those dollars can purchase over time.

Historical Benchmarks: How Tangible Bullion Insulates Capital

Gold has long been valued as a store of purchasing power because it is scarce, durable, and widely recognized. While it is not a guaranteed short-term hedge against inflation, it has a long history as a monetary asset during periods of economic uncertainty.

History also shows that paper currencies can lose purchasing power when money supply expands rapidly or public confidence weakens. Examples such as Roman coin debasement and the Continental Currency highlight why scarce assets have remained relevant across different monetary systems.

Unlike fiat currency, gold cannot be created through policy decisions. New supply requires mining, refining, labor, and capital investment, which limits annual growth. This supply constraint is one reason many families continue to study physical gold during periods of inflation and monetary uncertainty.

Central Banks Continue Accumulating Gold

Modern central banks continue to hold and buy gold despite the existence of sophisticated bond markets, digital payment systems, and global banking infrastructure. According to the World Gold Council, central bank purchases reached 863 tonnes in 2025, which remained historically elevated even though it slowed from the recent pace. 2

Central bank buying should not be treated as a personal recommendation for families. It does, however, show that physical gold remains relevant within modern reserve management discussions tied to currency stability, liquidity, and long-term monetary resilience.

For readers interested in a deeper examination of long-term purchasing power trends, see A 50-Year Historical Analysis of How Bullion Beats Official Inflation Metrics.

Comparative Capital Preservation Frameworks

Physical gold is not the only asset families use to protect purchasing power. Many compare it with real estate, cash, bonds, private businesses, collectibles, and digital assets, each with different risks, costs, and liquidity characteristics.

Real estate may offer income potential and long-term appreciation but can also involve taxes, insurance, maintenance, financing costs, and a slower sale process. Physical gold does not generate income, but it may offer simpler ownership, greater divisibility, and fewer ongoing management requirements.

Gold is widely recognized and generally liquid, but sale timing still depends on dealer availability, authentication procedures, market conditions, and buy-sell spreads. It should not be described as instant or friction-free to sell.

For readers comparing ownership costs, liquidity considerations, and maintenance requirements, the next article in this cluster examines those differences in greater detail: Real Estate vs. Gold Bars: Comparing Liquidity and Maintenance Costs in an Inflationary Market.

Evaluating Tangible Reserves Against Digital Currencies

Both physical gold and digital assets are often discussed as alternatives to fiat currencies, but they operate differently. Digital assets rely on software, networks, exchanges, and regulatory frameworks, while physical gold exists independently of those systems.

A gold coin or bar does not require internet access, software updates, or blockchain validation. Ownership is tied to physical possession rather than participation in a digital network.

Neither asset is inherently superior. Digital assets may offer portability and technological advantages, while physical gold has a long history of global recognition and acceptance. For families focused on preserving purchasing power, understanding these differences is often more important than short-term price movements.

Readers comparing these two approaches should also review Gold vs. Bitcoin 2026: Which Asset Provides True Protection During a Fiat Currency Crisis?

The Structural Impact of Negative Real Yields on Physical Tangibles

Negative real yields occur when inflation exceeds the return earned on cash deposits or debt instruments. In that situation, an account balance may grow in dollar terms while losing purchasing power.

This can change how retirement savers view physical gold. Gold does not pay interest, but when inflation outpaces paper yields, that disadvantage can become less important.

Gold does not automatically rise when real yields turn negative. However, the opportunity cost of holding a non-yielding tangible asset may shrink when inflation erodes the real return of cash-based holdings.

Readers interested in the mechanics of this relationship can continue with How Negative Interest Rates in 2026 Fuel Gold’s Purchasing Power.

Implementation Strategies: Secure Acquisition and Account Structures

Once families understand the role physical metals may play within a broader wealth preservation strategy, the next question becomes practical: which products should they study?

Common options include:

- Fractional gold coins

- One-ounce sovereign coins

- Small gold bars

- Larger bullion bars

Each category carries different premium structures, divisibility characteristics, storage considerations, and sale flexibility. Smaller products may offer easier partial liquidation because owners can sell a portion of their holdings without selling everything. Larger bars may reduce premiums per ounce but can be less flexible when only a small amount needs to be sold.

Understanding product recognition, mint reputation, premiums, spreads, storage arrangements, and verification procedures is often as important as monitoring the gold price itself.

Jefferson Gold’s phone-supported model is designed to help customers understand available products, pricing, storage choices, and delivery options without presenting ownership decisions as one-size-fits-all solutions.

Smaller denomination products can offer greater flexibility for buyers who prefer to build their holdings over time. For a closer look at this approach, see Fractional Gold Buying Guide: How to Accumulate Small Sovereigns and Sovereigns on a Budget.

Physical Gold vs. Paper Gold: Understanding the Difference

One key distinction in precious metals ownership is the difference between physical gold and paper-based gold exposure. Physical gold means direct ownership of bars or coins, either in personal possession or through an allocated storage arrangement. Paper gold includes ETFs, pooled precious metals products, mining-company shares, and other paper products linked to gold prices.

While paper gold can provide market exposure, it may involve management fees, custodial arrangements, and other intermediaries that do not exist with direct physical ownership. This does not make paper products unsuitable, but buyers seeking direct ownership often prefer physical bullion because it reduces reliance on institutions and market infrastructure.

This distinction becomes especially relevant during periods of monetary uncertainty, when some buyers prioritize direct possession of a tangible asset rather than indirect exposure through a paper-based product.

Incorporating Physical Bullion into Self-Directed Retirement Accounts

Some account holders use specialized self-directed retirement accounts to hold qualifying precious metals under specific regulatory conditions.

The Internal Revenue Code generally treats collectibles differently from retirement assets, but Section 408(m)(3) provides exceptions for certain coins and bullion that meet statutory requirements. For gold bullion, the commonly referenced standard is .995 fineness or higher, with specific exceptions for certain U.S. coins.

IRS guidance also states that qualifying bullion must generally be held by a bank or approved non-bank trustee, not personally by the account holder. Because the rules are detailed, readers should consult specialized custodians and qualified professionals before making retirement account decisions.

Jefferson Gold’s educational guide on how to open a gold IRA account provides a starting point for understanding how gold backed retirement accounts are commonly structured.

Precious Metals Retirement Planning

Precious metals retirement planning should be approached as an educational process rather than a predetermined formula.

Account holders considering physical metals often ask:

- Which products are permitted by the custodian?

- Where will the metals be stored?

- What fees apply?

- How are products authenticated and verified?

- What procedures apply to future sales, transfers, or distributions?

- Which professionals should review the account structure?

The objective is not to replace every traditional asset. Rather, it is to understand how physical bullion may fit within a broader wealth preservation framework after appropriate professional review.

Insured Home Delivery and Private Custody Frameworks

Many buyers prefer direct ownership through home delivery rather than retirement account structures. In these cases, shipping, storage, documentation, and insurance become important considerations.

A reputable dealer should provide insured shipping, tracking, delivery verification, and discreet packaging. Buyers should also establish storage plans before delivery, whether that involves a home safe, private vaulting, insurance reviews, or inheritance documentation.

Private custody offers direct control but also direct responsibility. Owners should consider storage, record keeping, insurance, succession planning, and eventual sale procedures before acquiring physical metals.

Securing Generational Stability Through Tangible Assets

Wealth preservation through gold begins with a simple observation: purchasing power matters more than the number displayed in an account balance. Throughout history, currencies have changed, monetary systems have evolved, and governments have expanded money supplies in response to economic pressures.

Yet physical gold has remained a recognized store of value across borders, generations, and monetary systems. Physical gold is not risk-free. Prices can rise and fall. Buyers must account for premiums, spreads, storage costs, insurance considerations, dealer selection, and market timing.

However, physical bullion occupies a unique position because it combines scarcity, durability, portability, and global recognition in a single tangible asset. It cannot be printed, digitally expanded, or created through monetary policy decisions.

Readers comparing long-term asset insulation strategies can review why physical precious metals remain part of many wealth preservation discussions during periods of inflation, debt expansion, and monetary uncertainty.

Have questions about buying physical gold or learning how a Gold IRA account works? Speak with a Jefferson Gold specialist to learn more about available products, pricing, storage options, and account education.