Concerns about inflation, government debt, and the future of paper currencies have pushed many Americans to look beyond traditional savings and bank accounts. Two assets often enter that conversation: physical gold and Bitcoin.

Both are viewed as alternatives to fiat currency. Both have attracted supporters who question the long-term stability of today’s monetary system. But they differ significantly when it comes to ownership, accessibility, volatility, and dependence on financial or technological infrastructure.

Price performance tells only part of the story. For many retirement savers and wealth-preservation buyers, the more important question is how an asset may hold up when confidence in banks, currencies, or financial systems comes under pressure.

That question becomes especially important during periods of economic uncertainty, when access, control, and reliability can matter just as much as market value.

Key Takeaways:

- Physical gold and Bitcoin address different risks during periods of financial uncertainty.

- Physical gold does not rely on digital infrastructure to verify ownership or exist as an asset.

- Bitcoin offers portability and digital scarcity but depends on technology, network access, and secure custody.

- During periods of financial stress, ownership structure, accessibility, and reliability can become just as important as market performance.

The Legal Reality of Fiat Deposits: Access, Insurance Limits, and Systemic Risk

Most Americans think of a bank account as cash they can access whenever they need it. Most of the time, that’s true. During periods of banking stress, however, insurance limits, access to funds, and the treatment of large balances can become more important.

In the United States, eligible deposits at FDIC-insured institutions are protected up to applicable limits. However, not every account is structured the same way, and balances that exceed insurance limits may involve additional considerations. 1

This is one reason some wealth-preservation buyers choose to hold a portion of their assets outside the banking system.

A physical gold coin or bar is not a bank deposit. It exists independently of the banking system, which is why ownership structure becomes part of the conversation during periods of financial uncertainty.

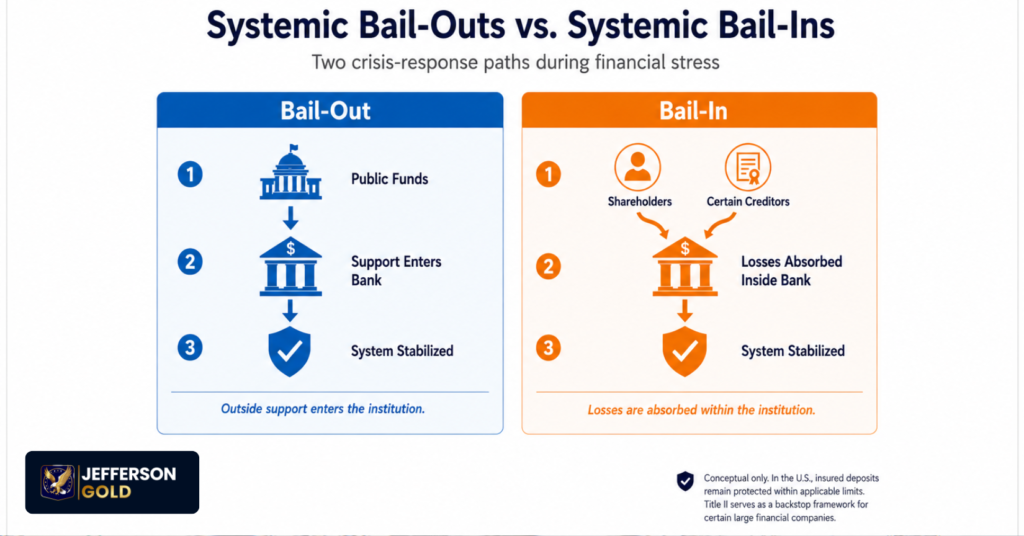

Dodd-Frank Title II and the Mechanics of Modern Institutional Bail-Ins

After the 2008 financial crisis, lawmakers introduced the Dodd-Frank Act, including a resolution framework known as the Orderly Liquidation Authority (OLA) for certain large financial companies. 2

This does not mean ordinary insured deposits are automatically converted during a banking event. FDIC insurance continues to protect eligible deposits within applicable limits, and bankruptcy remains the primary resolution process for most failing institutions.

The broader takeaway is simpler: different assets operate within different systems. Physical gold held directly exists outside the banking system, while bank deposits remain part of it.

For buyers focused on long-term wealth preservation, understanding those differences can be just as important as comparing performance.

Historical Precedent: What Cyprus Revealed About Banking Stress

The 2013 Cyprus banking crisis remains one of the most cited examples of how financial stress can affect account holders. As part of the country’s banking rescue, some uninsured depositors faced losses while smaller insured balances received different treatment.3

Cyprus does not predict what would happen in the United States, but it illustrates an important point: the structure of an asset can matter during a crisis.

A bank account, brokerage account, physical gold coin, and digital asset may all represent wealth, but they operate under different systems and rules. Understanding those differences provides useful context before comparing physical gold and Bitcoin.

Physical Gold vs. Digital Ledgers: Analyzing Structural Vulnerabilities

Physical gold and Bitcoin are often discussed together because both appeal to people who are concerned about fiat currency weakness. They are not issued by a central bank. They cannot be created by a government vote. They also sit outside the ordinary cash system.

But that is where the similarities begin to narrow. Physical gold is a tangible asset. A gold coin or bar can be held, stored, tested, transferred, and passed down without relying on a digital network. It does not need a password, internet connection, software wallet, or exchange account to exist.

Bitcoin is different. It is digital scarcity. Its supply is limited by code, and its network is designed to operate without a central issuer. That design is one reason many buyers see Bitcoin as an answer to fiat currency risk. Still, Bitcoin remains a digital asset. Practical access depends on electricity, internet service, devices, private keys, and the ability to use the network correctly.

That doesn’t make Bitcoin any less relevant. It simply means it offers a different type of protection than physical gold. For many buyers, the more important question isn’t which asset is scarce. It’s which asset they can still access and rely on if normal systems stop working as expected.

Power Grids, Connectivity, and Access During a Crisis

One of Bitcoin’s biggest advantages is that it can be transferred quickly across borders without relying on traditional bank wires. But access still depends on technology.

To use Bitcoin, owners need electricity, internet access, a secure wallet, and control of their private keys. During normal conditions, these requirements are easy to overlook. During a power outage, cyberattack, internet disruption, or exchange restriction, they can become much more important.

Physical gold comes with different considerations. It should be stored securely, and resale steps can vary depending on product type, documentation, custody history, dealer requirements, and whether the metal has been held directly by the customer or through a storage arrangement. However, a gold coin or bar does not depend on a network, software, or an internet connection to exist.

That difference helps explain why physical gold and Bitcoin are often viewed as complementary rather than identical forms of protection. One relies on digital infrastructure. The other does not.

Liquidity During Stress: Physical Custody vs. Digital Exchange Halts

Liquidity is often misunderstood in the gold versus Bitcoin discussion. Bitcoin can be traded around the clock, which gives it speed when exchanges, banking systems, and networks are functioning normally. During periods of market stress, however, exchanges may face outages, withdrawal restrictions, regulatory pressure, or other disruptions that affect access.

Gold liquidity works differently. Recognized gold coins and bars are bought and sold through dealers, vault networks, and private buyers around the world. Selling physical gold is not instant or cost-free, and factors such as dealer availability, product type, and market conditions can affect timing and pricing.

The key difference is that physical gold does not rely on a digital exchange to function. It can be sold through multiple channels, while ownership remains separate from a bank account or exchange balance.

Physical Gold vs. Digital Assets: Core Structural Comparison

Although both sit outside traditional fiat currency systems, physical gold and Bitcoin operate very differently when it comes to ownership, access, and resilience.

| Question | Physical Gold | Bitcoin |

| Form | Tangible Asset | Digital Asset |

| Scarcity Source | Geological Scarcity | Code-Based Supply Limit |

| Central Bank Issuance | No | No |

| Direct Bank Dependence | Not Required for Direct Ownership | Not Required for Self-Custody, But Often Used for Purchase or Sale |

| Infrastructure Dependence | Minimal | Requires Electricity, Internet Access, Devices, and Network Participation |

| Ownership Risk | Storage, Theft, Authentication, and Documentation | Private-Key Loss, Wallet Security, Exchange Risk, and Technical Error |

| Liquidity Path | Bullion Dealers, Coin Shops, Vault Networks, Private Buyers | Exchanges, Peer-to-Peer Transfers, Custodians, Payment Gateways |

| Volatility Profile | Historically Lower Than Bitcoin | Historically Higher Than Gold |

| Historical Monetary Use | Thousands of Years | Relatively Recent |

| Crisis Strength | Tangible Asset Outside Digital Systems | Portable Digital Scarcity When Networks Remain Available |

| Main Limitation | Storage and Physical Settlement Friction | Technology Dependence and Sharp Price Swings |

This comparison does not dismiss Bitcoin. Bitcoin has qualities that many buyers value: fixed supply, portability, and independence from central-bank issuance. It also gives self-custody options to people who are willing and able to manage private keys carefully.

But physical gold answers a different concern. Gold is not built for speed. It is built for endurance.

It has been used across cultures, governments, wars, currency changes, and banking crises because it does not require an issuer to stand behind it. For buyers focused on fiat currency crisis protection, that history still matters.

Gold, Bitcoin, and Volatility During Market Stress

Price behavior also matters. Gold can rise and fall. It is not immune to market swings. However, gold has often been treated as a reserve and safety asset during periods of monetary stress, geopolitical strain, or falling confidence in paper currencies.

Bitcoin has had periods of dramatic gains, but it has also had steep drawdowns. Its price can move sharply during broader risk-off markets, especially when speculative assets are being sold to raise cash. That volatility can be difficult for retirement savers who want stability, access, and long-term purchasing power protection.

A simple way to describe the difference is this:

Bitcoin may offer digital upside and portability, but physical gold has a longer record as a monetary safety asset. That is why the two assets should not be treated as interchangeable. They may both challenge fiat currency assumptions, but they do so in very different ways.

Questions to Ask Before Relying on Any Asset

A practical review of sound money assets in 2026 should begin with ownership and access.

A buyer can ask:

- Does this asset depend on a bank, exchange, or custodian?

- Can I access it if online systems are disrupted?

- Can I verify ownership without a third party?

- Can it be passed down clearly to family members?

- Does it have a long record of holding purchasing power through monetary stress?

- What friction exists when I need to sell or convert it?

- What storage, security, or technical responsibilities come with ownership?

Physical gold does not answer every need. It does not produce income. It must be stored carefully. Selling it may require authentication and dealer settlement. Bitcoin also does not answer every need. It requires technical care, private-key protection, and reliable digital access. It may also face exchange-level restrictions when a buyer wants to convert it through regulated platforms.

The real comparison is not “old asset versus new asset.” It is physical ownership versus digital dependence. For many Jefferson Gold readers, that distinction is the heart of the matter.

How Jefferson Gold Fits into the Physical Ownership Conversation

Many Americans looking at physical gold today are not trying to predict next month’s market movements. They are asking a more practical question: how much of their wealth depends on financial institutions, digital systems, or third parties continuing to function as expected?

Jefferson Gold works with families, retirement savers, and wealth-preservation buyers who want to own physical gold and silver directly. The company provides education, transparent pricing discussions, and access to precious metals for direct delivery or qualified retirement accounts. Jefferson Gold can also explain direct possession and allocated non-bank storage options for buyers who prefer to hold precious metals outside the traditional banking system.

For readers considering rolling over a retirement account into physical gold, Jefferson Gold offers educational resources that explain the process and available options. Readers researching why you should buy gold can also learn more about purchasing power concerns and the historical role of precious metals during periods of inflation and monetary uncertainty.

The focus is on helping buyers understand ownership, storage, and the practical considerations that come with holding physical assets.

Conclusion

Physical gold and Bitcoin both sit outside traditional fiat currency systems, but they solve different problems. Bitcoin offers portability and digital scarcity. Physical gold offers tangible ownership that does not depend on digital infrastructure to exist or be held.

For buyers concerned about inflation, debt, banking uncertainty, and long-term wealth preservation, that difference matters. Gold prices can fluctuate, and Bitcoin remains highly volatile, but access, ownership, and reliability may become more important than short-term performance during periods of stress.

That is why physical gold continues to be held by central banks, institutions, and families around the world. For those considering precious metals, the best place to start is understanding ownership, storage, and liquidity.