The relationship between negative interest rates and gold’s purchasing power is not simply a discussion about gold prices. It reflects a broader concern about what happens when cash and conventional yield-bearing accounts lose real purchasing strength.

In 2026, many American families and high-net-worth buyers are paying closer attention to real yields rather than headline interest rates. Even when savings accounts generate positive nominal returns, purchasing power can still decline if inflation rises faster than account yields.

In this context, gold’s purchasing power refers to what an ounce of gold can buy over time, not simply its quoted dollar price. That distinction matters because a rising gold price may reflect more than market demand; it may also reflect a weakening dollar, negative real yields, or declining confidence in paper-based savings.

This environment has renewed attention on physical gold. Unlike commercial bank deposits or conventional yield-bearing accounts, physical bullion does not depend on bank solvency, debt markets, or central bank rate policies to maintain ownership status.

For buyers focused on long-term wealth preservation, the discussion is no longer centered only on returns. It is increasingly centered on purchasing power, counterparty exposure, and the legal structure behind modern financial systems.

Key Takeaways:

- Negative real yields can weaken purchasing power even when account balances appear stable.

- Commercial bank deposits operate through a bank liability framework, not as segregated storage of the same physical cash.

- Physical bullion held with direct ownership may reduce exposure to institutional counterparty risk, while still requiring storage, verification, and liquidity planning.

The Mathematics of Negative Real Yields on Cash Reserves

The relationship between negative interest rates and gold’s purchasing power begins with a simple formula:

Real Yield = Nominal Yield – Inflation

If a savings account earns 3% while inflation rises 5%, the real yield becomes negative 2%. The account balance itself may still increase numerically, but the actual purchasing power of those dollars declines over time. 1

Why Purchasing Power Can Decline Even When Account Balances Rise

For many households, this loss appears gradually rather than all at once. The checking or savings balance may look stable, yet everyday costs continue rising in the background. Over several years, this erosion can materially weaken long-term purchasing power.

This is one reason physical bullion often receives renewed attention during periods of negative real yields. Gold prices can still fluctuate with market conditions, currency movements, geopolitical instability, and liquidity events. However, deeply suppressed real yields historically reduce the opportunity cost associated with holding non-yielding tangible assets.

Why Physical Bullion Draws Attention During Yield Suppression

The broader concern is structural rather than short-term. Traditional savings systems depend heavily on central bank policy, sovereign debt markets, and commercial lending activity.

When real yields remain below inflation for extended periods, many buyers begin reassessing whether conventional cash-based savings structures are preserving purchasing power in practical terms.

Physical bullion attracts attention during these periods because it exists outside the same credit and liability framework supporting modern banking systems.

The Legal Status of Bank Deposits: Unsecured Liabilities vs. Private Property

Many Americans understandably view a bank account as a secure storage location for personal money. Legally, however, commercial bank deposits operate differently from private possession of physical cash or tangible assets.

What Happens When Funds Enter a Commercial Bank

When funds are deposited at a commercial bank, the relationship is generally treated as a debtor-creditor relationship rather than simple storage of the same physical cash. In practical terms, the bank records the deposited funds as part of its balance sheet and owes the account holder repayment under the terms of the deposit agreement.

This structure is why the phrase bank deposit unsecured liability is important in systemic banking analysis.

The Debtor-Creditor Relationship Behind Deposits

Under standard commercial banking law, the relationship between bank and depositor is generally treated as debtor and creditor rather than bailor and bailee. In practical terms, the depositor does not retain ownership of the exact currency originally deposited.

Instead, the depositor holds a claim against the institution itself, which becomes legally responsible for repayment under the terms of the deposit agreement.

Why Deposit Classification Matters During Financial Stress

During normal economic conditions, most account holders never notice this distinction. During periods of institutional stress, however, the legal classification of deposits becomes more relevant because commercial bank deposits are handled through banking regulations, receivership rules, and administrative resolution processes.

FDIC insurance remains an important protection for eligible deposits up to statutory limits. However, deposit insurance does not alter the underlying legal structure of the deposit relationship itself.2

Commercial bank deposits remain institutional liabilities, while physical bullion held with direct title exists outside that banking liability chain.

Dodd-Frank Title II and the Structural Mechanics of Modern Resolution Authorities

Dodd-Frank Title II resolution authority established the Orderly Liquidation Authority, often referred to as the Title II OLA framework. This structure allows regulators to resolve certain large financial institutions outside traditional corporate bankruptcy proceedings when ordinary liquidation is determined to threaten broader financial stability.3

How Title II Resolution Authority Operates

Under a Dodd-Frank Title II resolution process, the FDIC may act as receiver for a covered financial company after required statutory findings are made. Regulators may transfer assets, establish bridge financial institutions, restructure liabilities, and continue critical operations while assigning losses according to statutory priority structures.

Understanding Single-Point-of-Entry Resolution

One of the central concepts within Title II OLA planning is single-point-of-entry resolution. Under this framework, losses are generally intended to be absorbed at the parent or holding-company level while operating subsidiaries continue functioning.

The goal is to stabilize the broader financial system while containing institutional panic.

For most Americans, these legal structures remain largely invisible during ordinary market conditions. However, they become highly relevant when examining how modern banking systems manage severe institutional distress.

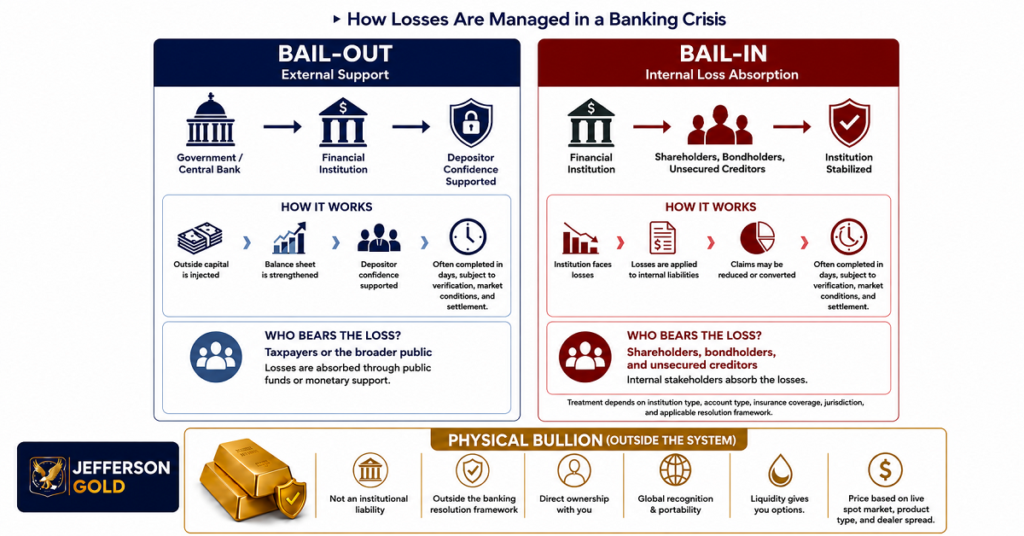

Bail-In vs. Bail-Out: Shifting the Burden of Solvency Interventions

The bank bail-in vs bail-out distinction explains how financial stabilization frameworks have evolved since the global financial crisis.

How Traditional Bail-Out Structures Function

A traditional bail-out relies on external support mechanisms such as sovereign borrowing, public capital injections, or central bank liquidity facilities. The institution receives stabilization support from outside its own balance sheet.

How Bail-In Structures Restructure Internal Liabilities

A bail-in restructures losses internally through the institution’s liability structure. Shareholders may be eliminated, certain bondholders may absorb losses, and unsecured claims may be impaired or restructured depending on the statutory framework involved.

Under modern resolution frameworks, the objective is often to stabilize critical banking operations while shifting a greater portion of restructuring pressure toward internal balance-sheet liabilities rather than external taxpayer-funded rescue mechanisms.

Historical Precedents: Institutional Balance Sheet Resolutions in Modern Banking

Several modern banking crises have demonstrated how access to deposits and institutional liabilities can behave differently during periods of severe financial instability. Cyprus and Greece remain two of the most widely referenced public examples.

The Cyprus Banking Intervention of 2013

The Cyprus intervention remains one of the clearest public examples of how modern banking restructurings can affect depositors and unsecured liabilities during periods of institutional instability.

In 2013, Cyprus faced a severe banking crisis tied to sovereign debt exposure and deeply weakened institutional balance sheets. As part of the stabilization process, uninsured depositors at certain banks absorbed losses through restructuring mechanisms tied to recapitalization efforts.4

The process introduced many global observers to the concept of internal liability absorption rather than traditional taxpayer-funded rescue structures.

What Greece’s 2015 Restrictions Revealed About Banking Access

Greece’s 2015 banking restrictions produced a different type of stress event. Instead of direct restructuring of deposits, the crisis involved a bank holiday, capital controls, withdrawal limitations, and temporary restrictions on banking access.

Even though balances technically remained in accounts, account holders faced operational constraints regarding access and transfer capabilities.

These events matter because they illustrate a broader point: access to funds and legal ownership structures can behave differently during periods of systemic instability than they do during ordinary economic cycles.

Physical Bullion Attributes as a Counterparty Risk Insulator

Several of these structural concerns help explain why some buyers look toward tangible assets held outside the traditional banking system during periods of monetary uncertainty and institutional stress.

Physical bullion differs from commercial bank deposits because ownership does not depend on a bank or financial institution repaying the account holder.

Why Direct Ownership Changes Counterparty Exposure

Commercial bank deposits represent institutional liabilities. Bonds depend on issuer repayment. Brokerage balances depend on custodial systems and digital financial infrastructure. Physical gold held with direct title exists independently of those intermediary obligations.

Why Physical Bullion Operates Outside Banking Liabilities

This distinction is why physical bullion is often discussed as a way to reduce exposure to institutional counterparty risk. The metal itself does not depend on commercial bank solvency, central bank liquidity facilities, or digital ledger continuity in order to maintain ownership status.

Gold’s historical role during periods of monetary instability is tied less to speculation and more to ownership structure. Physical bullion is finite, globally recognized, durable, and not created through bank lending or government currency issuance.

How Jefferson Gold Positions Physical Ownership Logistics

Jefferson Gold’s role within this framework is operational rather than promotional. The company helps customers understand acquisition logistics, delivery procedures, storage structures, and direct-title bullion ownership.

Readers reviewing asset insulation strategies can better understand how physical bullion differs from institutional financial claims, while those interested in direct ownership structures can review physical gold delivery procedures tied to tangible bullion acquisition.

Physical bullion is not free from operational realities. Storage planning, verification procedures, transaction spreads, shipping logistics, and secure handling remain important considerations.

However, these operational realities differ fundamentally from institutional counterparty exposure embedded within commercial bank deposits and other unsecured financial claims.

Direct Ownership, Control, and Liquidation Considerations

Direct title means the buyer owns the physical metal itself rather than holding a contractual claim issued by a financial intermediary. That distinction is central to physical bullion’s role in reducing counterparty exposure.

Physical gold remains globally recognized and highly liquid relative to many tangible assets, but liquidation is not instant or frictionless. Sale timing may depend on dealer availability, authentication procedures, market hours, shipping logistics, and prevailing bid-ask spreads.

Compared with commercial bank deposits, bullion ownership can reduce institutional counterparty exposure because the buyer owns tangible property rather than relying on a bank’s promise to repay.